Press releases

6 Mar 2024

With the brightest minds and the best technology, we can make your vision for card issuing, no matter how ambitious, a reality. Happy days.

How it worksJoin some of Europe’s leading voices to help settle the debate. Thorbjørn Fink, Chief Operating Officer, Pleo, Denmark’s youngest unicorn, Victor Kotnik, Partner in Consulting with Deloitte Sweden, Sharon Robson VP of Product Marketing at Enfuce and Philip Mikal Chief Product and Technical Officer at Enfuce.

Sign up now

We handle every aspect of card issuing and payments processing. Allowing you to scale your transformation programmes, quickly and easily, anywhere in the world.

As strategic partners, we champion your vision, offer practical, straight-talking advice, and go the extra mile to find the right solutions. Because when you win, we win.

Isn’t it nice to get exactly what you want and not pay for things you don’t? That’s why our platform is truly modular. It gives you the freedom to choose the optimum combination of capabilities that meet your needs, exactly.

We make it easy for you to scale your business and enter new markets. Our industry-leading cloud-based payments infrastructure is built to scale as your card and payment volumes grow. Simple.

Payment processing with an exceptional 99.999% uptime. Round-the-clock fraud monitoring. Dispute management, and PCI-DSS, GDPR, and PSD2 compliance. 3D Secure authentication… the list goes on. In other words, security’s taken care of.

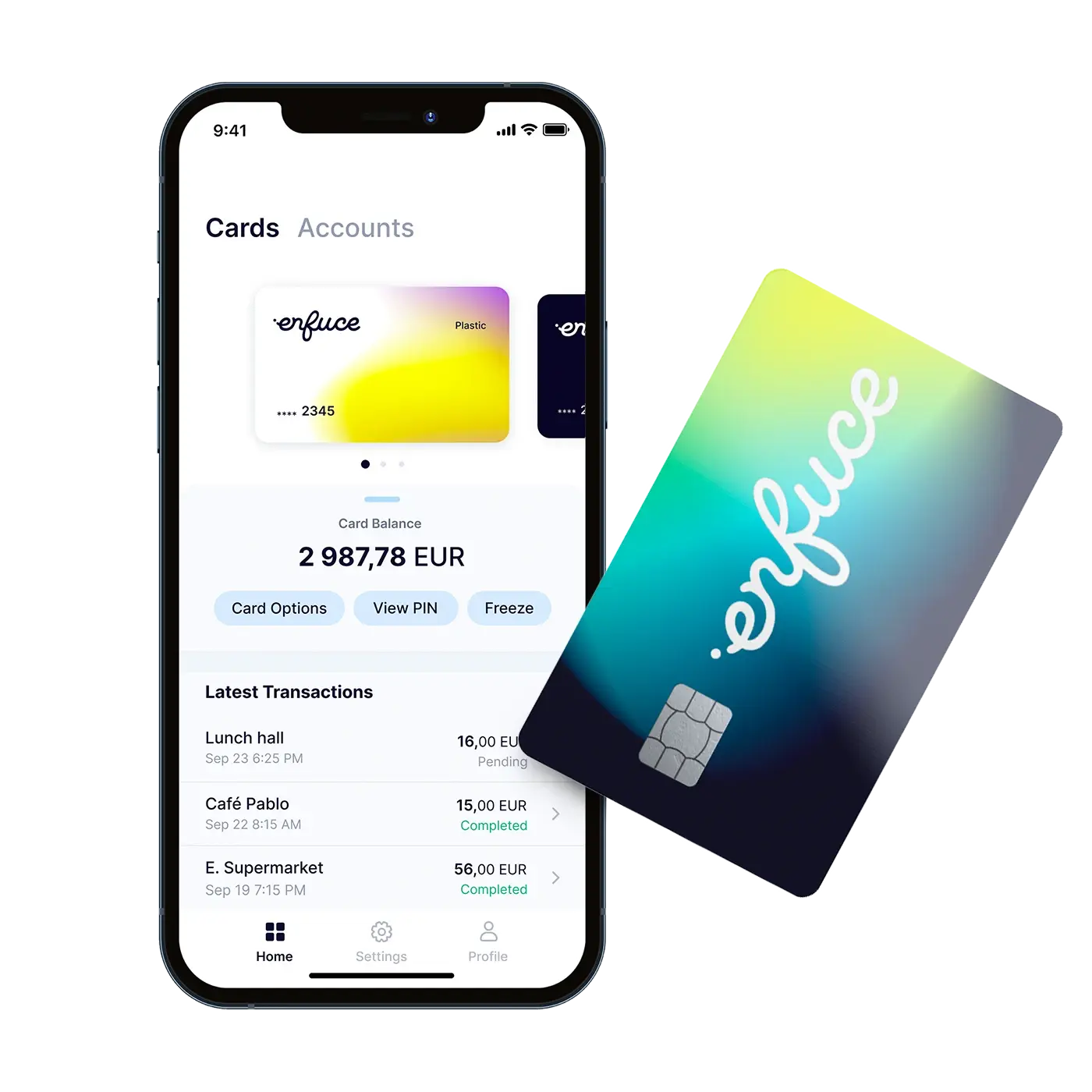

Card apps. Real-time data updates. Best-in-class payment processing. APIs that let you monitor card programmes, compare your performance, and share reports with important stakeholders. Who says you can have too much of a good thing?

If something’s needed, we sort it. Our open, honest dialogue constructively challenges expectations and supports your strategic decision making. Fusing first-class expertise and an entrepreneurial spirit, we stop at nothing to find the best solution for you. It’s that straightforward.

Discover your complete guide to successful card issuing. Everything you need to know to design a future-proof card product. The guide includes use cases, ecosystem partners, build vs buy considerations and more.

Download your copy