Card issuing API: How to scale your programmes compliantly

If you’re evaluating card-issuing APIs, you might be dealing with outdated infrastructure that’s slowing you down or manual processes creating friction. Or perhaps scaling your card programme has become more complex than expected. Ultimately, you’re looking for a solution that gives you the power to:

- Issue and manage virtual, physical debit, credit or prepaid cards via a single API

- Deliver reliable performance and uptime as volumes grow

- Expand into new markets without adding compliance or operational complexity

- Own the product experience end-to-end, with deep customisation and control

But not all card-issuing APIs are built the same. Some solve for speed but fall short on compliance. Others offer flexibility but struggle to scale reliably across markets. So how do you choose an API provider that won’t limit you as your programme grows?

As card issuers with over 10+ years of experience, we’re sharing our insights on when to integrate a card-issuing API, the key criteria for choosing a provider and how Enfuce can help.

Read on to learn:

- How does a card-issuing API work

- When to integrate a card-issuing API

- What to look for in a card-issuing API provider

- Why choose Enfuce to transform your card-issuing operations

- How Enfuce helped Swile issue 4 million employee benefit cards and scale across Europe and Latin America

Looking for a card issuing or processing partner? Contact us to see how Enfuce can help.

How does a card-issuing API work?

A card-issuing API connects your product directly to regulated payment infrastructure. Instead of relying on manual, bank-led processes, you can automate the creation, issuance, and management of virtual or physical payment cards through your own software. This gives you hands-on control without having to build complex card infrastructure from scratch.

With an API, you can plug into capabilities that have already been built and tested by a specialist provider. This makes it faster and more cost-effective to launch, while still allowing you to configure cards, spending rules, and programme features in a way that fits your business needs.

Modular card-issuing APIs may also include processing capabilities, handling authorisation, authentication, clearing, and settlement beyond card issuance alone. This means you can manage both issuing and transaction processing through a single platform, rather than integrating multiple systems.

Card-issuing API: An example

Here’s a quick example of how an API works for card creation with Enfuce:

- Customer data collection and onboarding. You, as the issuer, remain responsible for collecting and managing customer information and handling onboarding. This typically includes KYC/KYB checks, screening, application processing, and possibly creditworthiness assessments. After onboarding, the customer (the entity to which a card and/or an account is issued) and the account (the entity that holds the balance) are created in Enfuce’s system. Cards must be linked to an existing customer and account, so this step establishes the foundation for everything that follows.

- Your application triggers a card issuance request to Enfuce via the API. This request sends over all essential card details, such as whether it is a Visa, Mastercard or branded card, whether it is physical or virtual, which customer and account it should be linked to, the card’s role as a main or supplementary card, and the cardholder’s name. Optional fields can also be included to provide further detail, such as specifying a particular card design.

- Card creation. Enfuce creates the card and automatically links it to the defined customer and account. At this stage, any product-specific rules and features are applied automatically. These are based on the card programme configuration, and include elements like permitted transaction types, fee types, usage limiter types, BIN ranges, and expiration periods.

- Both physical and virtual cards are available for use immediately after issuance. Card details such as the primary account number, expiration date, and CVV can be accessed straight away for e-commerce transactions, and cards can be enrolled into digital wallets like Apple Pay or Google Pay as soon as they are issued. To support digital wallets, you must integrate with the relevant scheme tokenization services, which Enfuce’s Digital Wallet Module can manage for you.

Ongoing management, monitoring, and security. Enfuce provides a comprehensive suite of card management and payments APIs that empower you to manage the full lifecycle of customers, accounts, and cards, configure programme-level features, access reporting and insights, and implement controls. You also have full access to your (non-sensitive) data via APIs and data export files.

Caption: Enfuce’s card lifecycle management

Learn more about how to issue payment cards with Enfuce’s API in our full guide.

When to integrate a card-issuing API

Integrating card issuance into your existing infrastructure is particularly effective if you need to:

- Connect your card programme to core systems and applications, allowing customer and transaction data to flow automatically into reporting, accounting or compliance workflows.

- Issue cards instantly during onboarding or programme enrolment to ensure users can access funds or services without delays caused by manual issuance, batch processing, or provider-dependent setups.

- Set and update spending rules and limits in real time, enabling you to respond immediately to operational needs or policy changes. For instance, you may need to change per-employee allowances, merchant category restrictions or daily spend limits.

- Manage multiple card types or customer segments – such as corporate vs. retail users, or prepaid vs. credit cards – each with distinct controls, fees, or reward structures, without building everything in-house or relying on siloed providers.

- Enable real-time authorisation to approve or decline transactions based on your own rules and criteria.

- Access alerts, audit logs, and settlement and dispute reporting easily to support compliance, fraud prevention, and operational oversight.

- Offer multi-currency or cross-border cards, without having multiple providers or separate systems for each market.

Common scenarios where a card-issuing API can provide the most value include:

- Banks, fintechs, and digital-first lenders issuing debit, prepaid, or credit cards to serve retail, SME, or corporate customers

- Fleet and mobility providers enabling payments for fuel, charging, tolls, or vehicle-related expenses

- Merchants and employers delivering employee benefits, allowances, or stipends through prepaid or virtual cards

- Expense management platforms providing corporate cards tied to employee spending

- Non-profits and government organisations distributing aid or benefits quickly and securely to individuals or households

What to look for in a card-issuing API provider

To support these use cases, look for more than basic issuing capabilities. Here are the key areas to evaluate in an API provider:

Can you configure the API to your needs?

Look for the ability to actively configure card types, issuance methods, and product features to match your use case.

It’s also worth checking whether the API allows limits, controls, funding rules, and reporting workflows to be set programmatically, rather than requiring manual or provider-side changes. That kind of flexibility makes it easier for your card programme to evolve as your business grows, such as if you need to tailor controls for a specific customer segment or adjust rules for an expansion into a new market.

How easy is it to go from build to launch?

A strong card-issuing partner makes onboarding straightforward for technical teams. This includes comprehensive developer docs, clear API references, and a free sandbox environment where developers can test example code and see what card issuing looks like before going live.

Make sure there’s upfront clarity around what’s included out of the box, what’s optional, and which capabilities can be added later. This helps you avoid surprises when your programme launches and ensures the provider can keep up with your growth plans.

If you don’t have your own issuing license, you’ll also need a clear route to get one, either through your provider or via BIN sponsorship from a trusted partner. The ideal API provider makes this process straightforward, so you can focus on building your product rather than navigating licensing hurdles that delay your programme launch.

Are compliance and fraud prevention built into the platform?

Launching a debit, credit or prepaid product means navigating PSD2, AML, PCI DSS, GDPR, and scheme requirements – often across multiple markets. Look for providers that embed these requirements into their platform, such as PCI DSS Level 1-certified infrastructure and integrated fraud prevention tools.

Also, consider whether the provider has undergone regular audits, penetration tests, security reviews and vulnerability scanning. These hygiene factors protect you and your customers and remove the burden of regulatory overhead from your team.

Is there strategic alignment beyond the API?

Successful card programmes rely on more than technology alone. They require close collaboration across technical, operational and compliance teams. Choose a provider that understands your industry, compliance constraints, and growth plans – and is willing to co-create and evolve your card programme with you. The strongest partners help you design solutions tailored to your operations and goals, rather than forcing you into a rigid, one-size-fits-all implementation.

Why choose Enfuce to transform your card-issuing operations

Enfuce is a secure, compliant card issuing and processing platform that handles every aspect of card issuing and payments processing.

Our API-first, cloud-native solution combines the speed and efficiency of a ready-built system with the flexibility to customise, configure, and control your products. We handle the infrastructure, scheme access, and regulatory and compliance guardrails, while you remain in control of your customer journey and product features.

Here’s what you can do with Enfuce as your card-issuance partner:

Grow operations with an API-first solution that scales with you

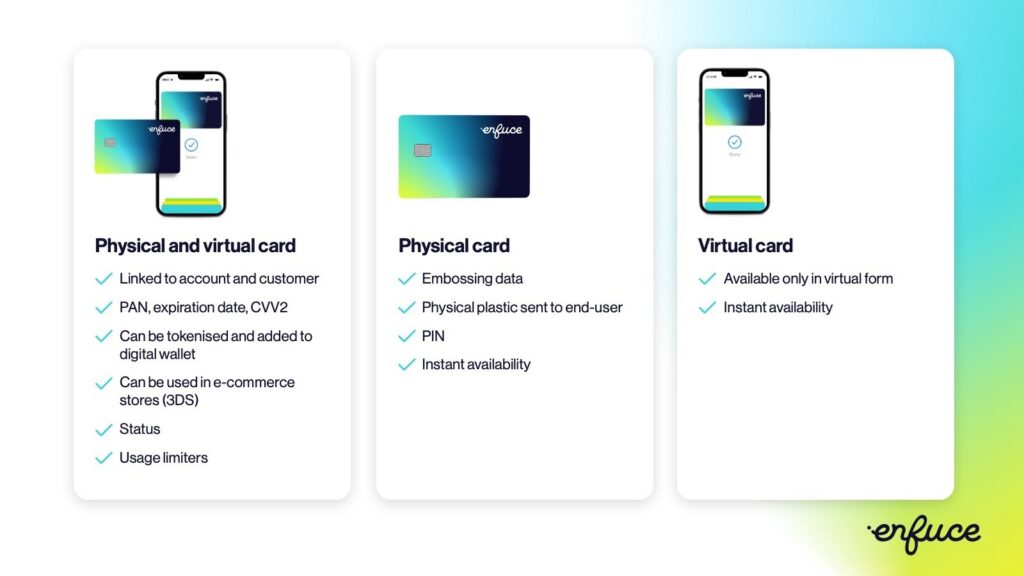

If you’re relying on legacy tech or an in-house system, agility can feel impossible. Testing new repayment journeys or rolling out differentiated products often comes with slow timelines, high costs, and operational risk. Scaling to new markets can be even trickier, with downtime, compliance, and performance limitations frustrating both teams and customers.Enfuce is designed to solve these challenges. Our cloud-native, modular platform handles thousands of transactions per second, supports scalable issuance ranging from 10,000 to 10 million cards, and lets you launch debit, prepaid, or credit cards from the same backend, through the same APIs.

Caption: Card product types in Enfuce

This flexibility allows you to test, launch, and scale different card products without changing platforms or adding vendors. For instance, you can start with prepaid for testing, add debit later, or launch country-specific credit cards in parallel – all with our solution.

With Enfuce, scalability and reliability are built in. Our stand-in processing (STIP) ensures uninterrupted availability of issuing and processing services. It can authorise transactions even during downtimes, replaying them once your systems are back online.

Tenant isolation is a security measure that further ensures our customers’ data and services are physically separated, so heavy traffic or issues on one account don’t affect others. This setup improves performance, enhances security and gives you more control over configuration changes.

In short, Enfuce delivers full-featured card issuing that’s flexible, secure and ready to scale with your business.

Manage multiple markets and currencies compliantly and without fragmentation through a single provider

Operating across multiple markets or business lines can quickly result in fragmented technology stacks. For instance, you might end up with different processors for each product, siloed data and compliance processes that don’t talk to each other.

This ultimately results in operational inefficiencies, from duplicated work across teams and slow reporting to delayed product launches and inconsistent customer experiences.

Enfuce simplifies this by being a single card-issuing solution that provides support for multiple markets. You get:

- Pre-integrated multi-country, multi-currency capabilities

- Support for local BINs and scheme and invoicing requirements, with KYC/KYB and customer activation aligned to local regulatory needs

- Market-specific reporting with stakeholder-ready data for reconciliation, compliance, and operational insights

As a dual-regulated Electronic Money Institution (authorised by both the Finnish FSA and the UK FCA) and a principal member of Visa and Mastercard, Enfuce also ensures your card programme is scheme-compliant and audit-ready from day one.

Our key compliance and fraud management features include:

- Scheme-certified onboarding journeys

- 3D Secure service

- Cross-border payment regulation

- PCI DSS Level 1 infrastructure

- Integrated fraud rules and alerts

- Automated dispute workflows

- Country-specific invoice templates and grace period logic

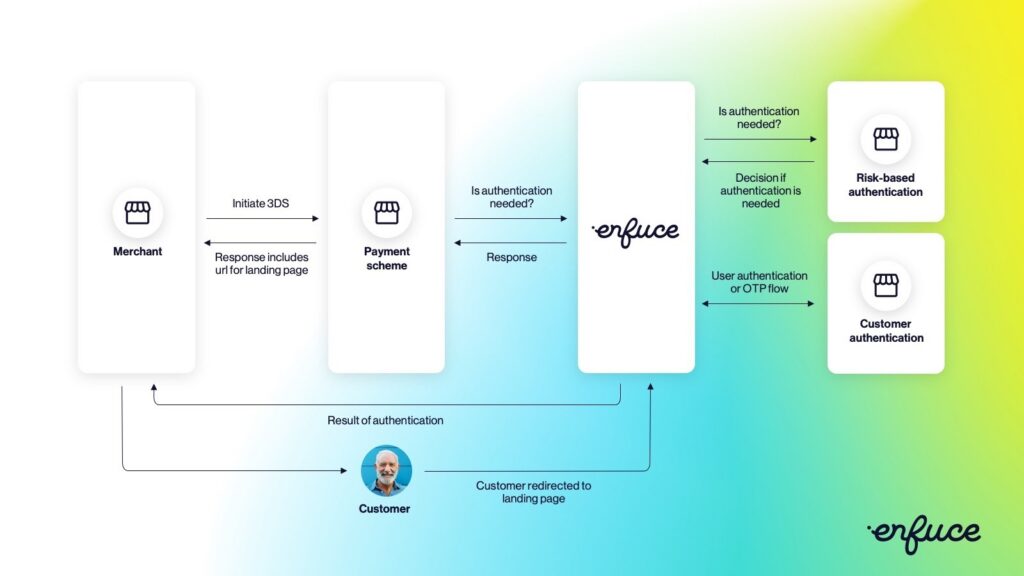

Caption: How 3D Secure works with Enfuce

All of this is accessible via Enfuce’s portal and APIs, so you get full transparency and auditability without needing to build it all yourself.

With Enfuce, multi-market card programmes are no longer fragmented or complicated. Instead, you get one compliant platform that can easily scale with your business.

Build a custom card programme in weeks with expert support

Your card programme should move at your pace. That means owning your product roadmap – from defining repayment logic and adjusting billing cycles to launching customer loyalty features and testing new ideas – without waiting on third-party approvals.

Enfuce’s modular, API-first platform lets you launch what you need today and layer in complexity as your strategy evolves. Plus, you only pay for what you use, making it a smart balance between rigid standardisation and costly customisation.

Want to see how it works? Developers can explore our Card details API in our sandbox. Just create an account for free to get started.

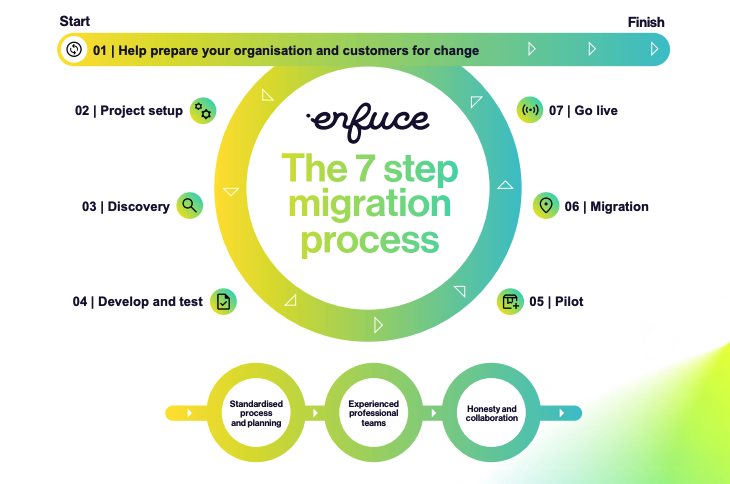

Beyond offering you control, we recognise that scaling a card programme across products and markets can be complex. That’s why Enfuce works closely with you every step of the way. Our team is here to help you build solid business cases, advise on best practices – including navigating EU regulations – and ensure you’re using our API to its full potential.When migrating your existing card programme to our API-first platform, you’ll work with our team to ensure your logic, operational workflows, and value-add features move with you. Together, we’ll coordinate testing, clarify responsibilities, and keep operations running smoothly – so you don’t have to carry the burden alone.

Caption: Enfuce’s 7-step migration process

The result is a solution that empowers your business to move fast, innovate safely, and deliver a seamless experience to your customers.

How Enfuce helped Swile issue 4 million employee benefit cards and scale across Europe and Latin America

Swile is one of France’s largest and most innovative employee benefit providers, processing €3 billion in transactions per year. The company had already disrupted the traditional paper voucher system by digitalising lunch vouchers and aimed to go further with a streamlined employee benefits experience.

Rapid growth and global ambitions posed a challenge: Swile needed an issuer processor that could scale reliably across multiple markets.

In France, Swile chose Enfuce to support its transition to becoming a licensed issuer. Leveraging our modular, cloud-native platform, Swile built a unique card that consolidates multiple benefits – from meals to mobility and culture vouchers – into one standalone card.

French employees can use the card online, in store, or via digital wallets – just like a regular payment card. Meanwhile, employers stay in control with sophisticated authorisation rules, purchase restrictions, and real-time approvals that keep spending aligned with company policy.

With employee benefits being a highly regulated product, compliance was critical. Enfuce’s technology is fully compliant, providing detailed reporting and linking each card to its own ledger to ensure funds are correctly allocated.

According to Swile’s Payments Product Director, Quentin Vigneau, the collaboration proved “instrumental in [Swile’s] ability to move fast across multiple geographies with an iterative approach to innovate.”

After a successful launch in France, Swile scaled rapidly, including a recent expansion into Latin America, introducing a multi-pan combo card, merging two of the most sought-after benefit categories, meal vouchers and multibenefit allowances, into one sleek solution and issuing over one million cards in Brazil. Enfuce’s scalable infrastructure and advanced compliance features made this possible, supporting more than four million active employee benefit cards and enabling Swile to continue innovating without operational bottlenecks.

Read more about how Enfuce and Swile are revolutionising employee experience management.

Take control of your card programmes with API-first infrastructure

Today’s card programmes need to be fast, flexible, and compliant by design – but legacy processors and fragmented systems make that hard to achieve. Enfuce removes these barriers, giving you programmatic control and the ability to scale across markets without added complexity.

Enfuce delivers this through an API-first, cloud-native platform that provides infrastructure, scheme access, and compliance guardrails – while you stay in control of the product experience and roadmap.

Ready to transform your card programme? Contact us today and see how Enfuce can power your next-generation card products.

FAQs about card-issuing APIs

What is a card-issuing API?

A card-issuing API connects your product directly to regulated payment infrastructure, enabling you to create, issue, and manage payment cards. Instead of relying on manual, bank-led processes, you can embed card issuance, controls, and lifecycle management directly into your own systems and workflows.

Which types of cards can I issue using a card-issuing API?

With a next-generation card-issuing API like Enfuce’s, you can issue virtual and physical cards and tokenized cards, including prepaid, debit, and credit cards. Cards can be configured with real-time spending controls, support multiple currencies, and be used online, in-store, or via digital wallets, such as Apple Pay and Google Pay, giving you full flexibility across use cases and markets.

How quickly can I launch a card programme with Enfuce?

Timelines depend on your use case, markets, and regulatory requirements. That said, Enfuce is purpose-built to accelerate time to market. With our modular, API-first platform, built-in compliance, and direct scheme access, many customers can move from solution mapping (and migration planning) to live card issuance in weeks rather than months, without compromising on control, security, or scalability.