How to switch issuer processors: A detailed card migration guide

If you’re thinking about switching issuer processors for your card programme, you may be looking for a provider with improved performance, more flexible technology or capabilities that better support your growth.

Perhaps your current setup with your existing processor is limiting your ability to scale, and you’re struggling to launch new products quickly enough to compete with more agile players. Or you may need infrastructure that can adapt to evolving regulatory requirements as your programme expands.

Whatever the driver, switching issuer processors isn’t something to take lightly. Without careful planning, migration can introduce operational risk, from temporary service disruptions to compliance challenges. That’s why having a structured migration approach – and the right partner – is critical.

With years of experience supporting large-scale issuer processing migrations, Enfuce understands what it takes to transition card programmes safely and efficiently. We have supported large-scale migrations across Europe and the UK, where careful preparation, collaboration and a structured framework make all the difference.

In this step-by-step guide, we’ll break down how to plan and execute a successful issuer processor migration. Read on to learn:

- How to switch issuer processors: 7 key steps

- What you need in place to switch issuer processing providers

- What to look for in a new issuer processing platform

- Why choose Enfuce when you’re ready to switch issuer processors

- How Enfuce and Avida migrated 500k+ card customers in 7 months with zero downtime

- FAQs

Want hands-on guidance? Talk to our team about switching issuer processors.

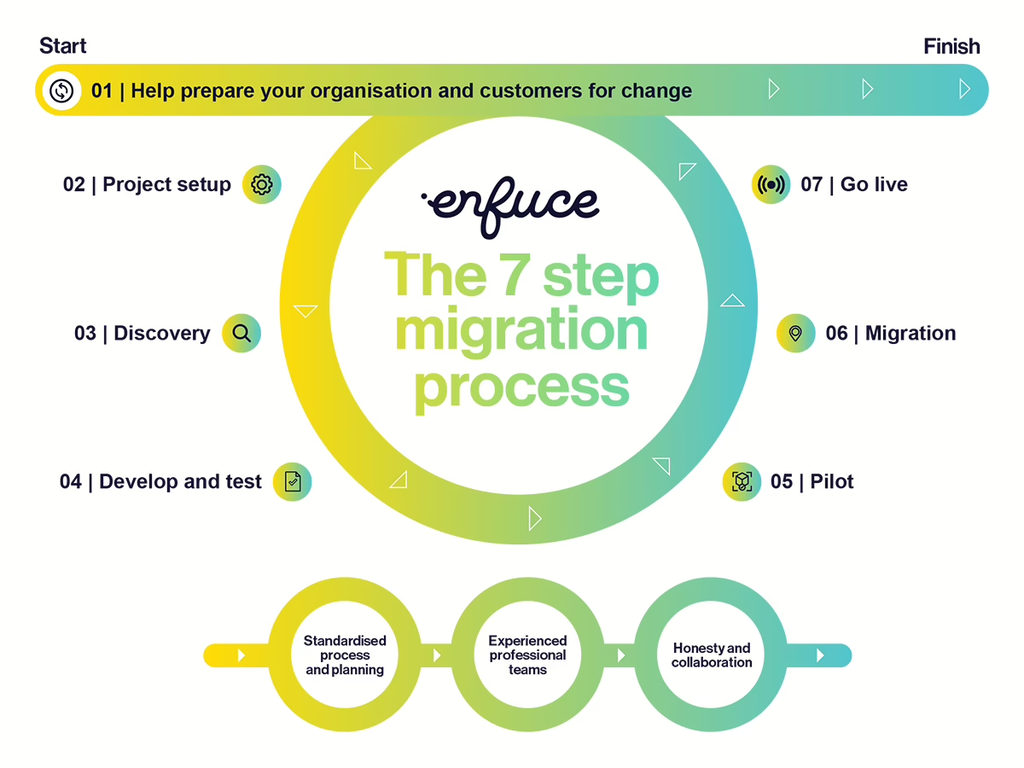

How to switch issuer processors: 7 key steps

Migrating a card programme to a new issuer processor is a major undertaking that requires careful planning and coordination. Here’s how our migration experts recommend handling an issuer processing switch:

- Prepare for change: Migration impacts every department: operations, risk, finance, customer service, legal, external partners and customers, and even marketing, when it comes to brand reputation. Map how your processes, reporting, and customer touch points are going to change in the new system, and come up with a plan to inform and prepare the stakeholders affected.

- Set up a dedicated migration team: Bring your team leaders and your new issuer processor’s migration experts together into a hybrid team. Define scope, timelines, milestones, stakeholder touch points, escalation paths, and transaction volume considerations.

- Discover and map data: Together, map your current setup in detail – product configurations, ledger configuration, fee structures, interest models (if applicable), customer data, repayment flows, and CRM integrations. Identifying and reviewing every data field, dependency, and edge case can help ensure accurate replication or optimisation.

- Develop and test: Tailor your programme to your business strategy and ensure you get sandbox access, full API specs, and a secure environment for testing. You’ll integrate apps, systems, and vendors, set up security keys and scheme integrations, then run end-to-end tests covering authorisations, statements, fees, interest, digital wallets, operational tools, and edge-case scenarios.

- Pilot and validate: Run a controlled live pilot with a small set of real cards to verify activation, transaction processing, billing or settlement flows, and overall customer experience across channels.

- Execute: Migrate static data (such as cardholder profiles and account information) alongside sensitive card data such as PANs through scheme-approved transfer processes, typically in defined waves with rehearsals and validation checkpoints.

- Go live and monitor: Once migration goes live, authorisation, clearing, and transaction processing shift from your previous provider to your new issuer processor. During the initial period, teams typically enter a “hypercare” phase, where operations are closely monitored using operational monitoring dashboards, and supported by rapid-response teams and enhanced incident tracking.

Want to learn more? Check out the full details of our seven-step guide to smooth card programme migration.

What you need in place before switching issuer processing providers

Before switching issuer processors, it’s essential to understand why you’re making the change and how your current card programme operates. You don’t have to have all the answers, but understanding your current setup and future goals will make planning and execution smoother.

Here’s what’s helpful to have in place before you begin:

- Define what you want to achieve. Pinpoint the challenges with your current issuer processor. Is support inconsistent? Are certain features missing? Is pricing misaligned? Knowing your desired outcomes will help you assess whether a new issuer processor can better support your ambitions.

- Align the right teams and define ownership. Make sure internal stakeholders understand why you’re switching and are ready to support discovery and change. When everyone knows the goals and their role, it’s easier to collaborate and keep the migration on track.

- Choose the right migration approach Every migration is different. Do you prefer a low-risk, phased transition or an all-at-once “big bang” migration? Consider your tolerance for running two systems at once, potential service interruptions or downtimes, and the preparation effort required. Knowing your preferences early will help you hit the ground running with the approach that fits your business.

- Know where your data lives. A successful migration starts with a clear view of your data. Migration typically requires transferring customer data, card account information, and ledger records. Find out where your information is stored and how it can be transferred securely. Is your data spread across several systems? Will it have to be migrated via API, files, or transformations?

- Identify connected tools and vendors. Issuer processors rarely operate in isolation. Your issuer processor may link to CRMs, onboarding tools, fraud detection systems, and other service providers that support your card programme. Mapping these integrations early helps identify what needs to be connected or configured during migration.

What to look for in a new issuer processing platform?

When evaluating a new issuer processing platform for performance and long-term growth, asking the right questions upfront helps determine whether your new partner can deliver lasting value:

- Does the platform align with your technical architecture and commercial strategies? Is the issuer processor API-first? Can it support your required volumes, authorisation speeds, and product complexity? Look at uptime metrics, SLA performance, multi-market payments support, and the ability to scale across markets.

- How reliable is it in practice? Look at real performance. Ask about incident history over the past year. What went wrong, how was it resolved, and how transparently was it communicated? A strong partner should demonstrate clear processes for incident management, recovery, and transparent communication.

- Do you have access to the right experts ? Consider whether the issuer processing platform can connect you with compliance and regulatory-reporting experts. Can they help you navigate complex requirements and offer consultation when you need it?

- Is compliance built into the platform? Look for a provider with strong regulatory credentials, such as an EMI licence and principal membership of major card schemes (Visa, Mastercard). This signals deep experience with regulatory compliance and scheme reporting obligations. Even if you operate under your own licence, you can gain peace of mind by having a licensed partner who embeds compliance into operations.

- Can the platform evolve with the market? A future-ready partner stays ahead of vertical-specific requirements and helps you adopt them without disruption. For example, if you’re in fleet and mobility, you may want to check that the issuer processor supports fleet-grade transaction data and controls aligned with scheme standards, such as Visa Fleet 2.0.

- Will they be a flexible, collaborative partner? Migration is complex. Choose a provider willing to build adaptation layers, tailor solutions, and actively guide you – not just give you access to their APIs without guidance or implementation support.

Why choose Enfuce when you’re ready to switch issuer processors

Enfuce is a regulated card issuer and payment processor operating across Europe, the UK, and South America.

Our modular, white-label platform is built to scale with you, whether you’re transforming an existing portfolio or launching a completely new programme. With a team of 150+ experts, we prioritise collaboration to help our customers access future-ready card features and build payment solutions with ease.

Here’s what you can do when you switch to Enfuce:

Upgrade performance and expand your card capabilities

If your current issuer processor struggles with downtime, slow issuance, or rigid features, innovation becomes difficult and growth slows. Enfuce helps remove these limitations, delivering reliable card operations while giving you the flexibility to evolve your programme.

Our cloud-native platform is built to stay up and scale with you, delivering 99.999% uptime. It also includes practical features that add an extra layer of resilience:

- Stand-in processing (STIP) that helps ensure transactions can still be authorised if the primary ledger system is temporarily unavailable.

- Tenant isolation to help ensure traffic spikes or issues from other programmes don’t impact yours.

You also don’t need to worry about slow card issuance. With Enfuce, you can issue physical or virtual cards instantly and enable tokenisation for mobile wallets, letting users make e-commerce purchases without delay. Our Digital Wallets module supports scheme tokenisation for Apple Pay, Google Pay, and other wallets, so you can focus on serving your customers instead of managing technical details.

As your business grows, Enfuce makes it easy to expand into new use cases without switching providers. For instance, you can:

- Support consumer and commercial cards across prepaid, debit, and credit models

- Offer flexible credit options, including revolving credit, charge cards, and instalment-based credit programmes

- Configure payment allocation rules, interest models, and advanced spend controls

- Set real-time authorisation rules to control exactly when, where, and how cards are used

- Leverage multi-currency and multi-country capabilities out of the box

Transition to a modular, cloud-based issuer processor platform with built-in compliance

Performance alone is not enough if legacy systems or manual processes limit your ability to move quickly. Future-proofing a card programme requires infrastructure designed to evolve alongside the payments ecosystem.

With Enfuce, you can migrate your issuing and processing to a cloud-native, API-first platform while staying in full control. Our modular architecture gives you the flexibility to start small, pay for what you use, and scale capabilities as your programme grows.

This setup lets you experiment with new features and launch multiple card products from the same backend. You can test new ideas, expand into new markets, or adapt to changing customer needs without the need for additional infrastructure changes.

Test it out yourself: Create a free account to access our sandbox and explore our APIs – like our Card details API or Spend Control API.

At the same time, compliance and risk management are built in and continuously updated. With Enfuce, you get:

- Built-in support for key European requirements, including PSD2, Strong Customer Authentication (SCA), and Cross-Border Payments Regulation (CBPR)

- A card payment processor that’s assessed annually and certified for PCI compliance (PCI DSS Level 1 and PCI 3DS)

- 24/7 real-time fraud monitoring as part of Enfuce’s modular platform

- Dispute management service, in which issues and disputes are handled in line with scheme and regulatory requirements

Get hands-on support driven by a dedicated team and our proven 7-step migration framework

Switching issuer processors can introduce operational risk if it is not carefully planned. Service disruption, compliance issues and customer friction are common challenges without the right expertise.

With Enfuce, you can migrate with confidence, knowing you have an experienced partner with you every step of the way.

Our proven seven-step migration framework combines structured planning with hands-on expertise to make transitions smooth and predictable. Whether you want a gradual, portfolio-by-portfolio approach or a larger, high-impact migration, the process is tailored to your preferences.

From the outset, you’ll have a dedicated team that works side-by-side with you to design the migration path. With years of handling large-scale, complex migrations across Europe and the UK, our experts know how to avoid common pitfalls and keep transitions on track. This framework has been proven in high-stakes environments, including Avida’s large-scale portfolio integration, completed in record time.

How Enfuce and Avida migrated 500k+ card customers in 7 months with zero downtime

When Avida acquired Santander’s sales finance and credit card portfolio, it faced the challenge of integrating hundreds of thousands of customers into its existing ecosystem without disrupting service. Avida chose Enfuce to lead the integration and ensure a smooth transition for all clients.

In just seven months, from contract signing to full completion, Avida and Enfuce successfully migrated over 500,000 customers – including 556,039 consumer credit cards and 94,009 installment plans – without zero service interruptions. This became one of the largest and fastest credit card migrations completed in the Nordics.

The migration’s success highlights the effectiveness of Enfuce’s structured seven-step migration framework. Careful planning, thorough testing, and close collaboration ensured that the team carried out every stage, from data mapping to go-live, safely and with precision.

Mikael Johansson, CEO of Avida, described the partnership: “From the very beginning, the cooperation has been characterised by a positive atmosphere and strong teamwork. Dedicated to deliver. Successfully migrating a card portfolio of this scale in such a short time is a remarkable achievement.”

Read the full story on how we accomplished this record-breaking Nordic card migration.

Switch issuer processors with a proven partner like Enfuce

With Enfuce, you gain a dedicated migration partner and a powerful issuing and processing platform built for growth.

Our cloud-native, API-first system delivers 99.999% uptime, modular capabilities, and granular controls that let you launch diverse products and scale without friction. Along with our hands-on migration support and deep regulatory expertise, you’ll get both a smooth transition and a future-proof foundation for your programme.

See how we can help you switch issuer processors. Get in touch today.

FAQs about how to switch issuer processors

How long does it take to switch issuer processors?

Migration timelines depend on portfolio size, complexity and the chosen migration strategy. Most migrations take several months to plan, test, and execute the transition in phases. That said, with a disciplined and structured approach, the process can move fast. Enfuce, for example, helped Avida migrate over 500,000 cardholders in less than seven months, from contract signing to completion.

Can you switch issuer processors without downtime?

Yes, it’s possible to switch issuer processors with minimal or zero downtime. Achieving this requires thorough planning, migrating data in stages, and rigorous testing to ensure readiness before the migration goes live.

What data needs to be migrated when switching issuer processors?

Migrating to a new issuer processor means moving all critical card programme data. This includes cardholder profiles, account balances, interest and fee settings, transaction histories, any connected systems, and sensitive data such as PANs and PINs, which require end-to-end encryption in order to maintain compliance with regulations . That’s why it’s important to know exactly where your data lives and how to access it before you start the