Expanding to a card-based EV payment solution: What you need to know

If you’re evaluating your current EV payment solution, you might be a mobility company like an e-Mobility Service Provider (EMSP), charging point operator (CPO), fuel retailer, or mobility provider that is facing deep structural challenges in how payments are managed.

Drivers often rely on a fragmented mix of apps, RFID tags, fuel cards and expense cards to pay for different services such as charging, fuel, tolls and parking. At the same time, regulations such as AFIR are pushing charging infrastructure to support ad hoc card payments, while increased interoperability between networks makes it easier for drivers to bypass proprietary solutions altogether.

Without a cohesive payment strategy, drivers may simply pay with their personal bank cards at the charger, weakening customer relationships, reducing access to transaction data, and limiting opportunities to build loyalty around your brand.

At Enfuce, we work with fleet and mobility companies navigating these challenges. In this article, we’ll walk you through why card programmes are becoming central to EV payment services, what to consider before upgrading your solution, and how working with a card issuing and processing partner like Enfuce can make life easier for your users while keeping your business future-ready.

Read on to learn:

- The challenges of EV payments and how card programmes solve them

- What to consider before upgrading your EV payment solution

- How Enfuce helps you future-proof your EV payments with card issuing and processing

- How Octopus Electroverse and Enfuce built a next-generation EV payments solution

- FAQs

Looking to upgrade your EV payment solution with a card programme? Enfuce is a global card issuer and payment processor that can help. Reach out today to learn how.

The challenges of EV payments and how card programmes solve them

EV charging payments remain highly fragmented. Drivers rely on a mix of apps, roaming platforms, RFID tags and direct card payments, often switching between different methods depending on the network or charging point they use. Charging infrastructure itself is not yet fully standardised, which means there is still no single payment method that works seamlessly everywhere.

However the industry is moving in that direction. Regulatory developments and rising customer expectations are pushing mobility providers to deliver simpler, more consistent payment experiences across charging networks.

Here is an overview of the main EV payment challenges affecting mobility companies, followed by how card programmes solve them:

Customer expectations

Drivers increasingly expect EV charging to be as simple as paying for fuel. Mastercard’s Electric Vehicles Payment Research found that 65% of respondents across seven European countries would prefer to pay with a card for each charging session. EVA England’s annual survey reported that drivers were frustrated over inconsistent payment processes and prices and desired universal contactless payment.

Visa has also highlighted the need for interoperable, seamless payment experiences across EV charging networks as infrastructure expands.

Regulations

Regulations are accelerating this shift by driving broader open-loop payment acceptance across EV charging infrastructure.

For example, AFIR in the EU mandates ad hoc payment options via card or contactless at public EV charging stations by 2027, and the UK’s Public Charge Point Regulations require most public charge points to accept contactless payments. While additional payment methods may still be supported, these regulations ensure that drivers must be able to pay using open-loop payment methods such as bank cards.

Operational pressure

Regulation is not the only force reshaping EV payments. Fleet and mobility companies are also facing operational pressure to simplify payments for mixed fleets. Many organisations are still transitioning from internal combustion engine vehicles to electric vehicles, meaning fuel and charging expenses must often be managed at the same time.

Managing mixed fleets becomes simpler when a single payment solution can be used for both fuel and charging.

Beyond that, customers value the ability to pay for other mobility-related expenses – such as parking, tolls and car washes – through one solution that works seamlessly across services and locations. For many fleet and mobility providers, this supports a broader goal of unified mobility spend management, where fuel, charging and other mobility costs can be tracked and controlled through a single payment system.

Current payment systems

Many existing payment solutions were not designed to support this level of flexibility. Scaling app-based or RFID systems across multiple services, locations and use cases quickly becomes complex.

At the same time, mobility providers still need to maintain strong spend controls, fraud protection and compliance as acceptance expands. Balancing these requirements is becoming increasingly difficult with fragmented payment systems.

Card-based programmes offer a way to address these challenges by combining the broad acceptance of payment networks with centralised spend controls, consolidated billing, and richer transaction data.

How a card programme solves EV payment demands

Card programmes provide a scalable payment infrastructure for mobility companies navigating fragmented payments and evolving charging regulations. By combining broad payment acceptance with operational controls (e.g., spend rules, reporting, consolidated billing) card programmes enable fleet and mobility providers to manage EV charging, fuel, and other mobility expenses through a single system.

With the right card issuer processor, you can build a card programme that:

- Supports ad hoc, open-loop payments required by regulations

- Scales across locations and charging providers more easily than apps or RFID alone, improving interoperability

- Consolidates payments for EV charging, fuel, and broader mobility services, accommodating mixed fleets

- Provides the controls, compliance, and fraud protections that align with your business strategy, including the ability to apply spend restrictions where required

What to consider before upgrading your EV payment solution

Introducing card-based payments can feel complex, but careful planning makes the transition significantly easier. Here are seven factors mobility companies should consider early:

1. Understand that card issuance comes with new regulatory obligations

Unlike RFID tags or mobile apps, issuing and managing payment cards is a regulated financial activity. This means you may need to adjust how you onboard cardholders, perform customer due diligence, and meet ongoing compliance requirements such as KYC.

2. Expect changes to your funds flow and cash management

In many existing EV charging payment setups, mobility providers settle charging sessions directly with charging point operators (CPOs) or through roaming platforms.

With an open-loop card programme, payments flow through the card network before being settled with merchants. Settlement timing may differ, which can affect cash flow and reporting. Understanding this early helps you adjust internal processes and avoid surprises at launch.

3. Consider what you want to handle in-house versus outsourcing

Decide what you want to control internally – such as the user interface and user experience – and what you prefer to outsource to experienced third parties, like issuing, payment processing, or KYC/KYB.

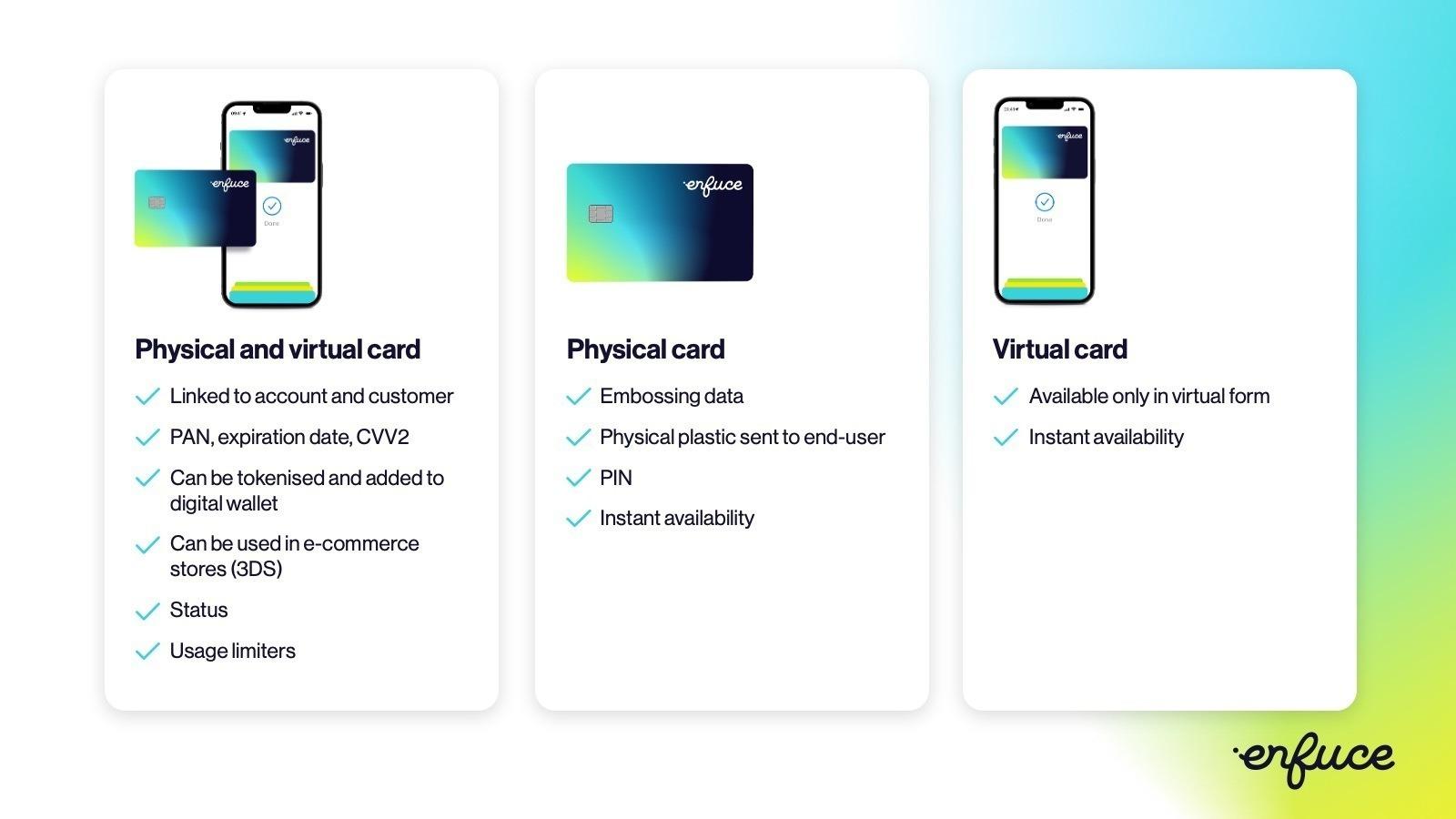

4. Start thinking about what type of card might work best

Prepaid, debit, credit, and charge cards each have different implications for cash flow, regulation, and partnerships (such as credit line providers).

5. Assess whether you want hybrid EMV and RFID functionality

Cards can support both EMV and RFID functionality, but performance depends on EV charging infrastructure, reader placement, and payment terminal technology.

Working with an issuer processor that supports diverse card types and has experience coordinating with card manufacturers and personalisation bureaus can help you understand trade-offs and identify the card type that best aligns with your strategy.

6. Decide whether you’ll get a license or launch via a BIN sponsor

This decision often starts with defining the role you want to play in the payments value chain and how you plan to serve your customers. Depending on your chosen role, you may decide to hold customer funds directly, operate as a payment service provider, or partner with licensed entities.

If you want to hold customer funds directly, you’ll typically need an EMI (or banking) licence; with BIN sponsorship, the licensed BIN sponsor/partner holds and safeguards funds.

7. Evaluate your issuer processor

Once your licensing strategy is clear, selecting the right issuer processor becomes critical. Ask whether they support the specific needs of EV and mobility payments. Look for configurable spend controls, real-time payment transaction visibility, flexible reporting and invoicing, scalable infrastructure, and experience handling regulated funds and complex settlement flows.

How Enfuce helps you future-proof your EV payments with card issuing and processing

Enfuce is a leading global card issuer and payment processor operating in Europe, the UK, and South America. We provide companies with the white-labelled technology and in-house expertise they need to create scalable payment card solutions.

Our modular platform is cloud-based and API-first, handling the full card lifecycle from issuing and processing to compliance. Beyond the technology itself, we take a hands-on, collaborative approach, working closely with you to tailor the setup to your business and ensure you get the most out of our APIs.

Fleet and mobility are core focus areas for us. We’ve helped companies like Shuttel and Octopus Electroverse launch card-based payment solutions that are compliant, convenient, and ready to scale.

Here’s how you can upgrade your EV payments to a card-based solution with Enfuce:

Protect customer loyalty by issuing future-ready cards with a modular, API-first infrastructure

With new EU and UK regulations requiring card payment acceptance at public charging points, traditional RFID tags and app-based payments may no longer be your users’ default choice. That’s loyalty – and your customer base – at risk.

With Enfuce, you can instantly issue virtual and physical EV charge cards, as well as enable contactless payments, to keep your users engaged with your brand. Launching is fast with our BIN sponsorship and EMI licence, which lets you bypass the need for your own e-money licence or scheme membership.

Our platform supports all card types – prepaid, debit, charge, and credit – through the same backend and reporting framework. This makes it easy for you to scale and introduce new products without changing partners.

At the same time, our processing capabilities enable you to run loyalty programmes, cashback offers, and targeted incentives based on charging behaviour. As a card issuer, you can also generate interchange revenue on every transaction – all without having to build and maintain the underlying infrastructure yourself.

Expand your payment solution with a unified card and multi-market support

Managing multiple payment solutions for EV charging, fuel, parking, tolls, and other mobility expenses can be complex and frustrating for both fleet managers and end users.

Enfuce makes it easy for you to issue a single, unified card that covers all mobility-related payments. You’re free to launch open-loop, closed-loop, or even hybrid card programmes. Our platform lets open-loop and closed-loop logic coexist for different customer segments behind the scenes, while your end users enjoy one consistent app or portal.

Scaling internationally is also straightforward. You can expand across multiple countries with multi-currency support, local BINs, and pre-integrated scheme invoicing. Through our strategic partnerships, you can also integrate vetted third parties for KYC/KYB, AML, credit scoring, customer onboarding, and more. No need to coordinate with multiple vendors at a time – you only need one platform to set up a fully compliant, ready-to-launch programme.

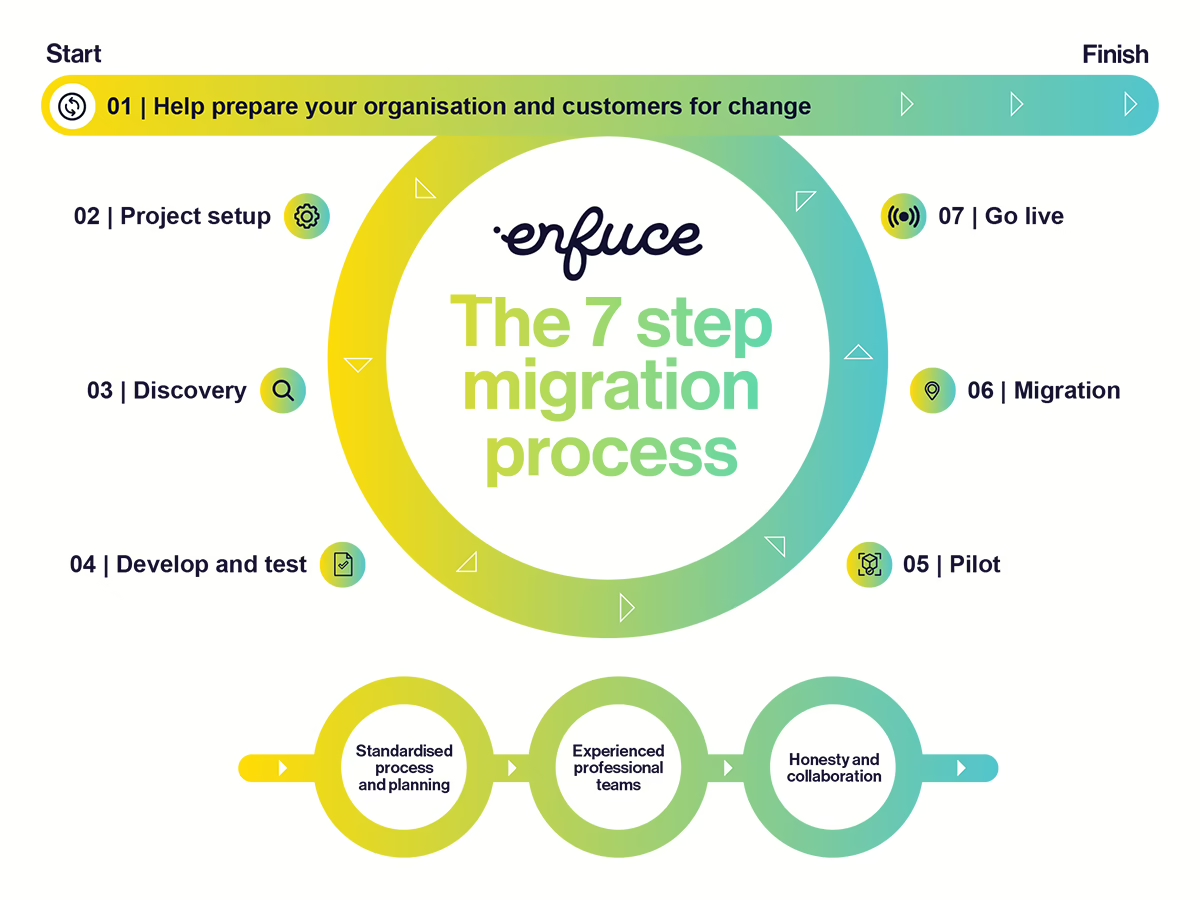

If you’re switching from an existing issuer processor, you can trust us to handle the transition with our proven seven-step migration process. You’ll work with mobility-focused platform experts who understand fleet operations, acceptance realities, and invoicing requirements, ensuring your solution is fully tailored to your business while your customers barely notice the switch.

Maintain control and compliance with advanced spend rules and fraud protection

Upgrading to an open-loop fleet or mobility card can raise questions about spend limitations, fraud protection, and compliance. If you’re used to restricted payment methods, it’s natural to worry that opening up to a wider network could reduce control over where and how cards are used or introduce new security risks.

With Enfuce, you maintain granular control over card usage. You can restrict cards to EV charging, fuel stations, parking, or any combination and build flexible rules for different user groups or business segments.

Our card-issuing APIs let you set advanced spend controls, including custom budgets, transaction limits, time-based rules, and restrictions by merchant category or geographical location. Curious how it works in practice? You can explore our Spend Control API, among others, in our sandbox by creating an account for free.

Compliance is built into our platform, so you don’t need to become an expert in card regulations. Enfuce is fully PSD2 and CBPR compliant and certified for PCI DSS Level 1 and PCI 3DS authentication. On top of that, we provide dispute management and 24/7 fully managed fraud prevention services as part of our modular offering, letting you focus on your business while giving your customers a controlled, compliant payment solution.

How Octopus Electroverse and Enfuce built a next-generation EV payments solution

Europe’s largest EV charging network, Octopus Energy’s Electroverse, connects EV drivers to over 960,000 EV chargers across 40+ countries through a network of more than 1,000 operator brands.

To simplify fleet payments and accelerate business electrification in the UK, Octopus Electroverse wanted to create a future-ready fleet payment solution – one that unified fleet expenses across charging, fuel, and everyday costs while supporting real-time spend controls and a digital-first user experience for hybrid fleets.

To do this, it needed a partner that could deliver end-to-end support, including scheme membership, regulatory compliance, and scalable infrastructure.

Octopus Electroverse partnered with Enfuce to launch the Electroverse Business Payments Card. Powered by Enfuce’s cloud-native architecture, the card is an open-loop Visa Fleet 2.0 solution that offers real-time spend controls, instant transaction monitoring, built-in compliance, and robust fraud protection.

Matt Pretorius, Head of Fleet Solutions at Octopus Electroverse, described the collaboration: “With a strong partner handling the complex work in the background, from BIN sponsorship to regulatory support, we were able to remain the masters of our own destiny. Bringing those strengths together in a true partnership is what has led us to where we are today.”

With Enfuce managing compliance, performance, and resilience behind the scenes, Octopus Electroverse can focus on what it does best: maintaining full control over its branding, customer experience, and customer relationships. The result is a robust, future-ready solution already delivering value and ready to scale.

Get the full story on How Octopus Electroverse is Powering the EV Revolution via our podcast.

Upgrade your EV payment solution with Enfuce

Issuing a card programme can help you align with evolving payment standards, simplify fleet management, and give users a seamless payment experience that consolidates EV charging, fuel, and other mobility services payments into one.

Enfuce’s modular, API-first platform makes it easy to issue a single card that works for fuel, EV charging, and other mobility expenses. You can set advanced spend controls to manage usage across different fleets or segments, while keeping fraud and compliance fully under control. And because our platform is built to scale, you can expand into new markets without building complex infrastructure or juggling multiple providers.

Ready to take the next step in upgrading your EV payment solution? Contact us today.

FAQs on EV payment solutions

What is an EV payment solution?

An EV payment solution is how drivers or fleets pay for electric vehicle charging. It can be in the form of a card, digital wallet, app, or RFID tag. Some solutions like cards now go beyond charging, letting users pay for fuel, parking, tolls, and other mobility expenses all via one payment method.

Why are flexible, card-based payments becoming more important in EV charging?

While EV charging payments are still fragmented, with inconsistent payment acceptance across networks and locations, regulations and customer demands are pushing for the universal acceptance of card and contactless payments at public charge points. This makes open-loop, card-based payments a strong foundation for greater consistency. They reduce friction for drivers, simplify fleet management, and enable a single way to pay for charging, fuel and other mobility expenses.

What should I consider before launching a card-based EV payment solution?

Moving to card-based payments can be a big shift, so it helps to plan ahead. Think about regulatory requirements, changes to how funds flow, and whether you want to handle card issuance in-house or work with a partner. Consider which card type fits your users best, and whether you want hybrid EMV and RFID functionality to support multiple charging hardware setups.

Let’s talk.