How to improve the cardholder experience: 5 tactics for issuers

According to the Capgemini Research Institute’s World Retail Banking Report, only 26% of customers are satisfied with their card experience. To build loyalty, increase retention, and stay competitive, issuers need to not only meet expectations but consistently exceed them.

But improving the cardholder experience requires more than surface-level changes. From how you handle compliance to the type of cards you offer, every layer of your programme shapes how cardholders perceive and engage with your product.

As a dual-licensed electronic money institution (EMI) and principal member of Visa and Mastercard, Enfuce has spent the last decade supporting fintechs, financial institutions, fleet and mobility providers, expense management platforms and enterprises in building card programmes designed around real cardholder behaviour and expectations.

Drawing on this expertise, we’ve identified five key ways issuers can meaningfully improve the cardholder experience, and what that looks like in practice.

In this article:

- 5 ways to improve your cardholders’ experience

- How to implement these strategies with Enfuce

- How Alisa Bank built a smooth cardholder experience with Enfuce

- FAQs

Enfuce is a cloud-native, API-first card issuing and processing platform helping issuers build customer-centric and secure card solutions. Contact us to learn more.

5 ways to improve your cardholders’ experience

When cardholders disengage, two problems often play a significant role.

The first is friction. From waiting days for a card to arrive to being repeatedly challenged on low-risk transactions when smarter, risk-based authentication could have let them through, these small but persistent inconveniences add up. Over time, they strain the cardholder relationship and give customers a reason to reach for another card.

The second is limited differentiation. When a product offers little flexibility and lacks relevance to how cardholders actually spend and manage money – for instance, lacking the ability to tailor spend controls, repayment models, or card use cases by segment – customers have no strong reason to stay loyal to one card over another.

Ultimately, improving cardholder satisfaction means delivering seamless digital experiences and building programmes that are tailored to real cardholder behaviour while also eliminating the friction that frustrates everyone. Here are five areas worth focusing on:

1. Design upgrades to be invisible to cardholders

Infrastructure upgrades are often what make better cardholder experiences possible in the first place. For instance:

- Expanding from a closed-loop to an open-loop system can increase acceptance, enabling cardholders to use their card beyond specific merchants or networks when required.

- Replacing a legacy platform with a cloud-native one makes it easier to roll out new features by enabling faster development and easier updates.

- Consolidating multiple programmes (e.g., bringing separate debit card, credit card, or regional card setups onto a single platform) can create a more consistent experience across products.

Delivering these kinds of upgrades could require migrating to a new issuer processor or platform. However, poorly executed migrations can introduce operational risks – like downtime, declined transactions, or app issues – that disrupt the very experience you’re trying to improve.

The challenge is realising the benefits of a migration without exposing cardholders to any of the risks. That typically comes down to careful planning, thorough testing, and a phased approach that validates each step along the way.

To learn more, read our guide on how to switch issuer processors while keeping the experience seamless for your cardholders.

2. Ensure compliance and fraud management without adding unnecessary friction

For issuers, compliance is non-negotiable, but the way it’s implemented can have a direct impact on the cardholder experience. Security measures that aren’t designed thoughtfully can easily introduce friction (and frustration) for your customers.

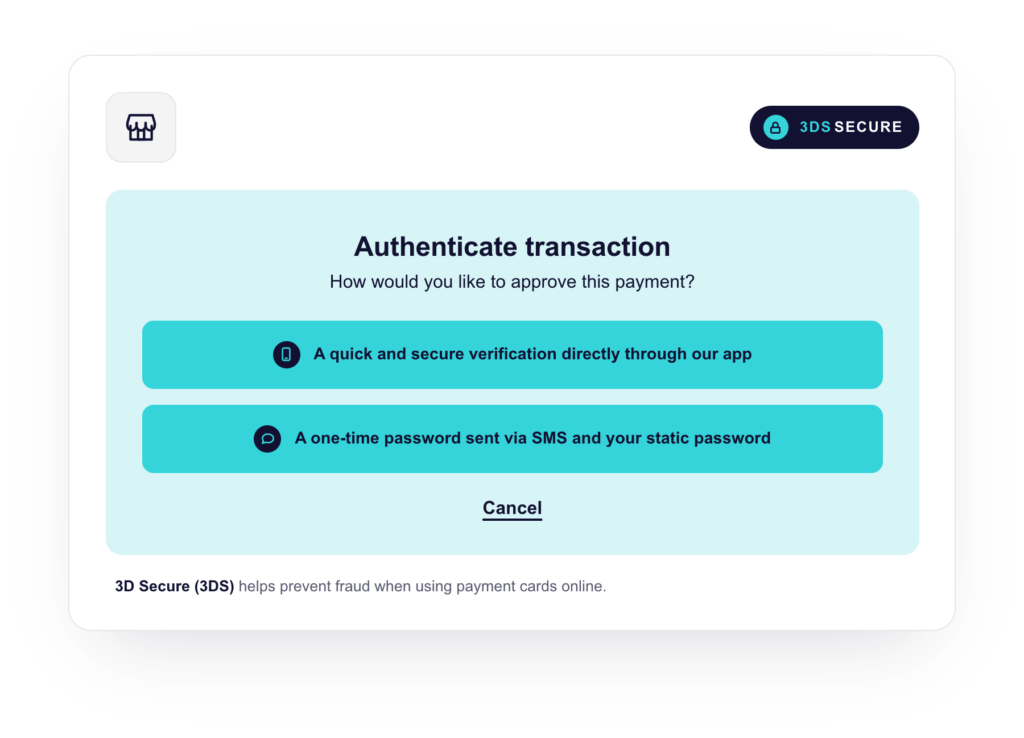

Take authentication. When cardholders are given only one way to verify their identity, that single option can become a blocker. An SMS one-time passcode is useless without cellular service, in-app prompts don’t help if the cardholder doesn’t have their phone on hand, and an email OTP creates unnecessary delay if they aren’t logged into their inbox.

Giving cardholders a choice of verification methods, so they can use whichever works for them in the moment, eliminates those potential bottlenecks and keeps the transaction moving without compromising security.

Similarly, fraud monitoring rooted in rigid, outdated rules can flag legitimate transactions as fraudulent. A better approach is for rules to be grounded in industry best practices and continuously refined using real cardholder behaviour and emerging fraud patterns. This ongoing optimisation helps reduce false positives without compromising fraud detection.

3. Provide a digital-first card experience

Cardholders increasingly expect to use their card as soon as they’re approved, rather than days later when a physical card arrives. Virtual cards and digital wallet integration meet that expectation by making cards usable straight away.

According to ABI Research, digital instant issuance is projected to nearly quadruple between 2023 and 2028, from 542 million to close to 2 billion. Additionally, 63% of consumers say they’d welcome their bank or card issuer pushing new cards to their mobile wallet (i.e., push provisioning), rising to over 71% among 18 to 37-year-olds.

That said, the majority of consumers (82%) see a continuing role for physical cards, reinforcing that a digital-first approach should prioritise flexibility rather than replace plastic altogether. Some cardholders will still want a physical card, just not necessarily at onboarding. Giving them the flexibility to decide later works better than forcing a single format.

Beyond access, cardholders also want more control over their cards and to exercise it digitally. Checking a PIN, freezing a card, receiving real-time notifications, setting spending limits, or reordering a card directly online or from an app is now an expected part of the cardholder experience. By enabling greater self-service, you reduce friction, improve customer satisfaction, and even take pressure off your customer support team.

4. Offer more flexible and personalised payment options

Nearly a third of cardholders now use card-attached instalment plans, a trend retailers and merchants have also taken note of, with a majority (76%) expecting consumer use of instalment plans to increase.

The value of features like instalment plans and post-purchase payment splitting is that they give cardholders more control over repayment and overall cash flow. That flexibility increasingly factors into which card they reach for.

Flexibility can also extend beyond the repayment model itself. Issuers can define spend controls by merchant category code (MCC), transaction amount, or location, adjust interest rates by segment or product, and vary grace periods based on how the card is used. This allows card programmes to reflect real card usage patterns and tailor products to different spending behaviours and customer segments.

The closer the card structure aligns with actual usage patterns, the more likely the card is to be used regularly and become a primary payment method.

5. Simplify everyday use with multi-card functionality

Cardholders often manage multiple cards for different purposes, like personal spending, business expenses, and specific benefits. That setup can be inconvenient: multiple cards to juggle, multiple PINs to remember, and more decisions to make at the point of payment.

Multi-PAN cards simplify this by combining multiple accounts onto a single card, each with its own balance and controls. At checkout, the cardholder can choose which one to use. For instance, they may charge a business lunch to a corporate account and then dinner to a personal account, all from the same physical card.

For the cardholder, that means greater convenience with fewer physical cards to manage. For the issuer, it’s an opportunity to offer a single card that strengthens cardholder loyalty with every account added to it.

How to implement these strategies with Enfuce

Implementing the above strategies depends largely on your infrastructure and the operational model behind your card programme. You can build these capabilities in-house, adopt a turnkey solution, or partner with a platform that already has the issuing, processing, and compliance infrastructure these strategies depend on.

Building in-house offers full control but comes with significant investment in scheme connectivity, regulatory compliance, and ongoing operations such as fraud monitoring and dispute management. Turnkey solutions, on the other hand, can accelerate delivery, though it’s important to consider how well they support your programme as your strategy evolves.

As a dual-licensed EMI and principal member of Visa and Mastercard, Enfuce provides issuing, processing, and scheme access within a single platform. This includes support for PCI DSS, PSD2, and scheme reporting, alongside operational services such as fraud and dispute management.

At the same time, our cloud-native, API-first architecture allows you to define how your programme is structured, configured, and scaled over time.

Here’s how Enfuce helps you enhance the cardholder experience:

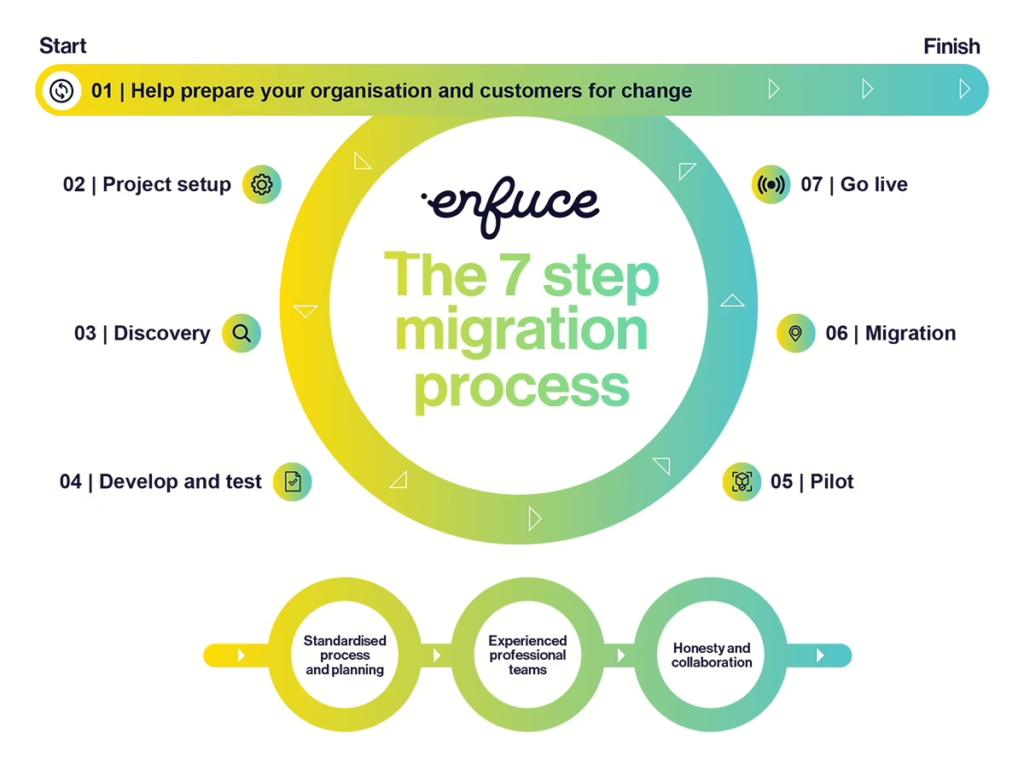

1. Migrate confidently with our structured, hands-on framework

Enfuce designs migrations to be predictable and tailored to your approach, whether you prefer a phased, portfolio-by-portfolio rollout or a larger-scale transition. Our seven-step migration framework combines structured delivery with hands-on expertise to minimise risk and reduce disruption for cardholders.

From the start, you work alongside a dedicated migration team that co-designs the transition path with you. This team brings experience from complex, high-volume migrations across Europe and the UK, helping you avoid common pitfalls and support a smooth transition.

For instance, Pleo, a spend management platform, had thousands of plastic and virtual cards in circulation when migration became necessary. COO Thorbjørn Fink credits Enfuce’s future-ready technology stack with making the transition feel manageable, and points to the team’s clear and constant communication as a standout part of the partnership.

2. Deliver secure, low-friction experiences with built-in compliance

With Enfuce, you can design card programmes that meet regulatory and scheme requirements without adding unnecessary friction to the user journey.

Compliance is embedded from the start, with built-in coverage for GDPR, PSD2, PCI DSS, and scheme rules, so you can operate with confidence across Europe and the UK. Enfuce also stands with the Fortitude Pledge, a compliance and security standard that aims to eliminate 100% of financial crime risks across all Enfuce-processed card transactions.

With our 3DS service, you can reduce authentication friction by offering multiple verification methods, including in-app authentication, SMS or email OTP, behavioural biometrics, and knowledge-based authentication. This flexibility gives your cardholders more choice and improves their experience, reducing authentication friction while supporting higher approval rates.

You’ll also have access to our 24/7 fully-managed fraud detection and dispute management services.

Our in-house fraud operations hub monitors more than 20 million authorisations monthly across 60+ live portfolios, scoring around 9.5 million transactions per month. This scale gives us deep visibility into fraud patterns through large volumes of transaction data and supports a 99.4% fraud detection rate.

Meanwhile, our dispute management service covers the full lifecycle, including chargebacks, write-offs, arbitration, compliance handling, and scheme reporting.

Together, this means fewer unnecessary declines, faster resolutions when issues do occur, and a smoother, more reliable payment experience.

3. Launch and control cards instantly across digital channels

With Enfuce, you can support a digital-first card experience by issuing both virtual and physical cards within the same programme.

Virtual cards are immediately usable for ecommerce and online payments from issuance, and physical cards can be added to digital wallets like Apple Pay and Google Pay as part of the initial signup flow, so they’re spendable even before the plastic arrives, and more likely to become the cardholder’s top-of-wallet choice.

Enfuce also enables a flexible “phygital” approach. Rather than locking users into a single format, cardholders can decide at any point in their journey whether to add or switch to a physical card, and change their decision over time.

To meet customer demands for greater control, you can embed card issuing and management directly into your own branded app or digital channels. That way, cardholders can securely access card details, set and retrieve PINs, and update them when needed. You can also enable other self-service controls, such as freezing, geo-blocking, cancelling, or reordering cards.

4. Create flexible repayment experiences that fit each cardholder

With Enfuce, you can design card programmes that align with how cardholders manage spending. You can support everyday financial flexibility with credit models like revolving credit and post-purchase instalment plans, so your cardholders can repay in a way that fits their lifestyle.

You can also tailor billing cycles, interest calculation logic, grace periods, minimum-to-pay (MTP) rules, and payment allocation priorities for different products or segments. That level of configurability means the product can be built to reflect how a specific type of customer earns, spends, and repays.

Qred, for instance, identified how traditional banking often falls short for small business owners with slow decisions and inflexible credit options. Launching its card product with Enfuce, Qred enabled SMEs to access a fast, transparent credit card solution tailored to their day-to-day needs.

The programme has continued to evolve, with new features introduced to better meet customer demands, including an invoice payment solution allowing customers to pay off their purchase invoices in a few clicks using the Qred VISA.

5. Unify multiple card programmes with convenient multi-PAN cards

With Enfuce, you can simplify complex card setups using Dual PAN and multi-PAN cards, which bring multiple card programmes together on a single physical card.

Instead of managing separate cards for different purposes, cardholders can access multiple accounts – lunch allowances, mobility cards, debit and credit accounts – through one physical card in their wallet. This creates a simpler (and more sustainable) experience: one card to carry, one PIN to remember, and fewer decisions at the point of payment.

Cardholders can customise the default payment method used for contactless payments, as well as the order and name of the different card PANs. At the point of payment, they simply select the relevant account directly on the terminal before confirming the transaction with their PIN. Each card application is linked to its own dedicated account and ledger, so spending is always correctly allocated without adding complexity to the cardholder’s day-to-day experience.

For you as the issuer, controls remain fully flexible. You can adjust limits, enable or disable specific card applications, and update rules in real time without reissuing a physical card.

How Alisa Bank built a smooth cardholder experience with Enfuce

For Alisa Bank, a Finnish digital bank, launching a Visa consumer credit card was central to expanding its digital banking capabilities.

Alisa Bank partnered with Enfuce to support its full card programme, including card issuance and processing, PSD2 open banking compliance, fraud monitoring, dispute management, and technical setup. This enabled the bank to focus on what mattered most: delivering a smooth, end-to-end cardholder experience.

As Juha Saari, Director of Personal Customers at Alisa Bank, put it, “When we started developing the card, the most important thing was to offer the smoothest customer experience on the market when applying for and using the card. Furthermore, we wanted the card launch schedule to support the overall launch schedule of Alisa Bank’s basic banking services. The cooperation with Enfuce has helped us achieve these objectives.”

Together, Enfuce and Alisa Bank delivered a fast, low-friction onboarding journey where customers can apply in-app and start using their virtual credit card immediately after approval, supporting a smooth experience from the start.

Read the full case study to see how Alisa Bank brought its credit card experience to market with Enfuce.

Build a better cardholder experience with Enfuce

Improving the cardholder experience depends on getting the fundamentals right across infrastructure, security, product design, and everyday usability. Enfuce gives issuers the technical infrastructure and expertise to turn that into a reality, helping them move faster and deliver better experiences without taking on unnecessary operational complexity.

Find out how Enfuce can help improve your cardholder experience. Contact us today.

FAQs on how to improve the cardholder experience

How can card issuers enhance the cardholder experience?

Issuers can enhance the cardholder experience by reducing friction and increasing flexibility across the cardholder journey. This includes seamless migrations, low-friction security, instant digital access to cards, flexible repayment options, and simplified multi-card setups.

Why is a digital-first card experience important for cardholders?

A digital-first experience allows cardholders to start using their card immediately after approval, without waiting for a physical card. It also enables greater control online or through mobile apps, such as freezing cards, setting limits, or managing PINs. This reduces friction, meets today’s expectations for speed and convenience, and improves overall satisfaction.

What is a multi-card or multi-PAN setup in card issuing?

A multi-card or multi-PAN setup allows multiple card accounts to be linked to a single physical card. Each account has its own balance and controls, but cardholders only need to carry one card and remember one PIN. At checkout, they can choose which account to use, which simplifies everyday payments.

Let’s talk.