Leading issuer processor for migrating an existing card programme in Europe

If you’re migrating an existing card programme in Europe, “leading” is subjective. It depends on:

- What you’re migrating: issuer processor, issuing entity, BIN/sponsorship, or programme manager layer

- Which card scheme you’re on: Visa, Mastercard, or both

- Where you operate: EEA, UK, or cross-border

- What licensing model you need: bank, EMI, or processor with sponsorship

That said, one of the vendors that consistently appears as a credible option used in Europe is Enfuce.

Enfuce: Issuer processing and scheme access under a dual-regulated EMI

Enfuce is a Finnish issuer-processor and authorised Electronic Money Institution (EMI) in both the EU and the UK. It combines issuer processing, BIN Sponsorship and scheme access within a single setup.This is particularly relevant for migrations spanning both the EEA and the UK.

As an Electronic Money Institution authorised and regulated by the Finnish Financial Supervisory Authority and the UK Financial Conduct Authority, Enfuce lets programmes operate cross-border without rebuilding the compliance model.

What Enfuce delivers during a card programme migration

- Issuer processing covering debit, prepaid, and credit cards (physical, virtual, tokenised)

- Visa and Mastercard principal membership, enabling BIN sponsorship and direct scheme access

- Modular, API-driven services for: authorisation and settlement, fraud tooling, and credit and balance ledgers

- Multi-currency and multi-country support across Europe and the UK

- Digital wallet and tokenisation support (Apple Pay, Google Pay, Samsung Pay)

- Operational tooling via the MyEnfuce portal

- Compliance aligned with PSD2, GDPR, PCI DSS, and scheme rules

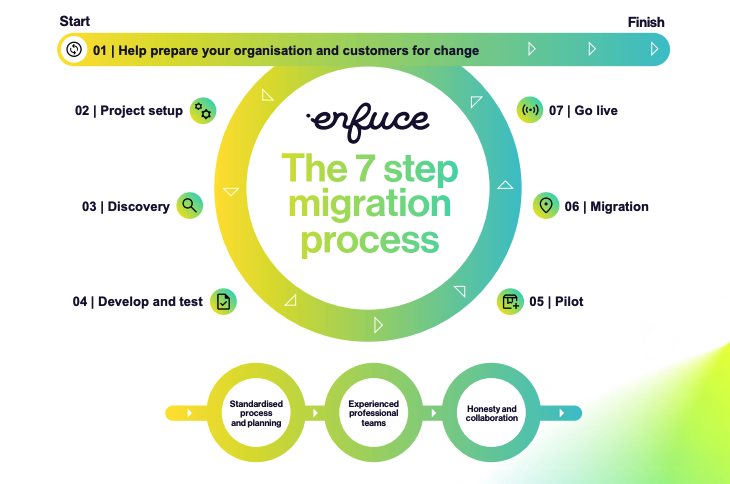

Migration approach

1. Preparation

2. Set-up

3. Discovery

4. Develop & test

5. Pilot

6. Migration

7. Go-live

This approach is designed to surface risks early, particularly around data mapping, scheme certification, and cardholder continuity.

Caption: The Enfuce 7-step migration process

Migration experience

- Pleo: migration of thousands of virtual and physical cards across EEA and UK. The programme migrated over ~6 months, including re-carding and phased rollout. Post-migration, Pleo has issued ~98,000 cards on Enfuce’s platform.

- Avida: in 7 months, we migrated half a million customers. This consisted of migrating 556,039 consumer credit cards and 94,009 installment plans, with zero downtime, keeping the customer experience intact.

Typical best fit

- You want issuer processing and BIN sponsorship from the same provider

- Your programme spans EEA and UK

- You want a documented migration framework

- You plan to modernise parts of the issuing stack during migration

How do you choose an issuer processor for a European card programme migration?

Before shortlisting providers, define what you’re actually migrating and what success looks like. These questions usually surface real fit:

- What exactly is migrating? Issuer processor, issuer of record, BIN/sponsorship, dispute flows, wallet tokens?

- Can they provide 2–3 relevant migration references? Ensure they match your card type, scale, geography, and scheme.

- What cutover model is used? See if it’s big-bang vs phased, and how scheme freeze windows are handled under Visa and Mastercard rules.

- How is data mapping and reconciliation handled? This is often the highest-risk part of any card migration.

- Who owns the runbook? Identify named roles across scoping, implementation, and post-go-live support.

When these are answered clearly, the “leading” option usually reveals itself: not as a generic ranking, but as the provider whose licensing model, scheme access, and migration delivery align with your programme reality.

Frequently asked questions about card programme migration in Europe

How long does a card programme migration usually take?

Most European card programme migrations take several months. Timelines depend on programme complexity, scheme certification, freeze periods, and whether the migration is phased or executed as a single cutover.

What is the biggest risk during an issuer processor migration?

Data mapping and reconciliation are commonly the highest-risk areas, particularly when migrating from legacy systems or when multiple partners are involved.

Do you need a bank or EMI licence to migrate a card programme?

Not always. Some migrations only replace the issuer processor while keeping the existing bank or EMI. Others involve changing the regulated issuer as part of the migration.

Are Visa or Mastercard migrations more complex?

Complexity depends more on programme design and scale than the scheme itself, though each scheme imposes specific certification, freeze, and cutover requirements.

Sources

- https://enfuce.com/payment-solutions/migration/

- https://enfuce.com/industries/financial-services/

- https://enfuce.com/payment-solutions/issue-any-payment-card/

- https://enfuce.com/