Card fraud detection: What card issuers need to know

Fraud tactics are evolving faster than ever, and so are the compliance rules designed to combat them. For card issuers, that means navigating challenges on several fronts:

- Fraud is moving faster than your systems can: Without real-time detection, fraudulent transactions slip through, driving up dispute volumes and cardholder complaints and damaging the customer experience.

- Fraud patterns vary by portfolio, region, and more: Without the right resources or in-house expertise, it becomes harder to interpret alerts and prioritise real threats.

- Card fraud detection becomes harder as your operations grow: Expanding into new markets, managing multiple programmes, and trying to stay current with the latest regulatory and scheme requirements make compliance harder, increase risk, and slow you down.

Together, these challenges turn fraud detection into an operational burden and strategic bottleneck, affecting customer experience, compliance, and your ability to scale.

As a card issuing and processing platform supporting fraud prevention and dispute management in multiple markets, Enfuce has helped clients achieve up to 5x lower fraud losses than comparable issuers. In this guide, we share our expertise and break down what card issuers need to know about fraud detection, from best practices to what to look for in a solution.

Read on to learn:

- How to detect and reduce card fraud

- What to look for in a card fraud detection solution

- How to reduce disputes and false positives with Enfuce’s fraud detection system

- Case study: From 315+ monthly disputes to a 70% reduction after migrating to Enfuce

- FAQs about card fraud detection

Contact us to learn how we can power your card programme, while managing fraud detection and dispute management for you.

How to detect and reduce card fraud

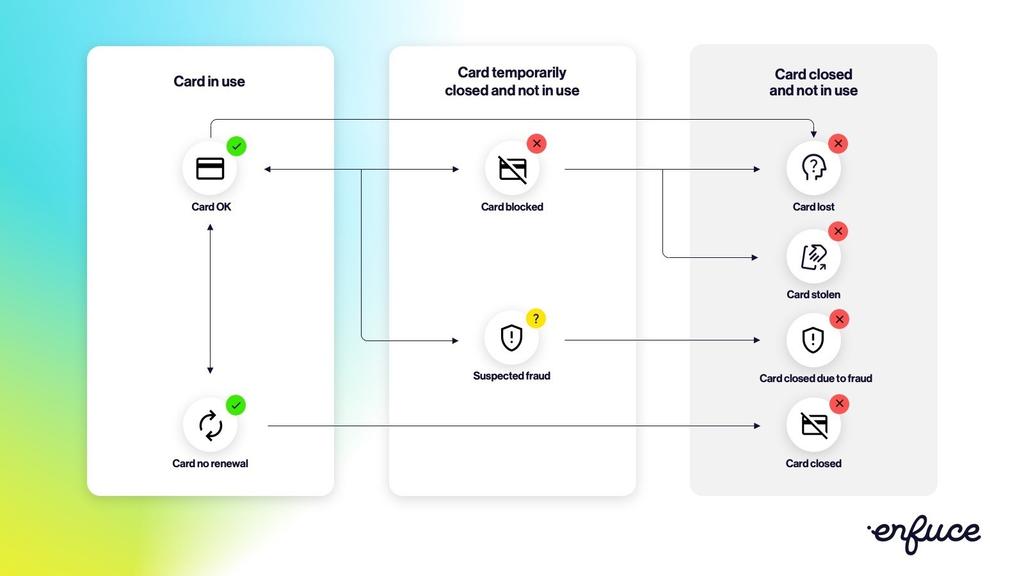

Card fraud occurs when a payment card and the underlying card information is used without the cardholder’s authorisation.

However, card fraud is no longer a static threat you can address with fixed rules or periodic reviews. For issuers, it’s a constantly shifting risk that requires real-time visibility, adaptive systems, and operational readiness.

Here are the steps to take to detect and reduce fraud as a card issuer:

1. Know the most common types of card fraud

Detecting fraud starts with knowing what forms it takes. The most common types of fraud to be aware of include:

- Card testing fraud: Scammers make small, low-risk transactions on stolen cards to ensure a card is active before making more significant purchases

- Card not present (CNP) fraud: Stolen or breached card data is used to make purchases at online or e-commerce merchants, where a physical card isn’t necessary

- Lost or stolen card fraud: A stolen physical card is used to make unauthorised transactions before the cardholder reports it missing

- Skimming and cloning: Card data is stolen via compromised physical terminals or ATMs and used to create a cloned card

- Account takeover: A fraudster gains access to a cardholder’s account (often via phishing or social engineering) and makes unauthorised transactions

- Card not received fraud: A new or replacement card is intercepted in the mail and used before it reaches the legitimate cardholder

- Fake or compromised merchant fraud: Transactions are processed through fraudulent or compromised merchant accounts to capture card data or launder funds

- Chargeback fraud: A cardholder makes a legitimate purchase but fraudulently disputes the transaction to get a refund while keeping the goods or service

Taken together, these fraud types highlight just how varied and fast-moving the threat landscape is, and why recognising them isn’t enough without the right foundations in place to detect and respond in real time.

2. Have the right fraud-fighting foundations in place

Fraud detection typically involves a dedicated fraud prevention team using advanced tools to monitor transactions and perform statistical data analysis. The goal is to identify patterns across large datasets and pinpoint where and when potential fraud has happened or is likely to happen.

Effective card fraud detection depends on having key elements in place, such as:

a. Artificial intelligence

Artificial intelligence (AI), machine learning and advanced algorithms are increasingly key to identifying patterns across data. Compared to traditional rule-based systems, which are static and can only catch what they’ve been explicitly told to look for, AI-driven systems improve the speed, automation and accuracy of fraud analyses by continuously learning from new data.

AI builds a behavioural baseline for each cardholder and flags anomalies as they emerge. This makes it better at detecting the kind of subtle, evolving fraud patterns that rigid systems miss.

b. Real-time customer and transaction data

Effective fraud detection requires a complete, real-time picture of each cardholder’s behaviour across payments, transactions, account-level changes, and device activity. The idea is to establish a baseline of each cardholder’s “normal” behavior, which allows for quick anomaly flagging.

This is especially useful in scam-driven fraud, where the cardholder is an active participant in the transaction. These cases are harder to detect using traditional rules, as the behaviour often appears legitimate. Detecting them requires systems that can identify subtle behavioural changes in real time, rather than relying on static or delayed signals.

c. Knowledge sharing

Some fraud patterns are widespread; others are niche and may only appear in certain verticals. Relying solely on your own portfolio gives you a limited view, making it harder to spot emerging threats early.

To stay ahead, issuers need a broader view. This means combining multiple sources of fraud intelligence, such as participating in industry forums or scheme-led knowledge-sharing initiatives, working with partners who monitor fraud across multiple programmes, and incorporating external data feeds into their detection systems.

However, building and maintaining this level of visibility independently takes time and resources, particularly as your operations scale.

d. Cardholder education

When it comes to fraud prevention, humans remain the weakest link. Training cardholders to recognise suspicious activity is an essential layer of defence alongside technical detection measures.

As an issuer, that means keeping cardholders informed on a continuous basis with in-app prompts, timely notifications, and clear, consistent communications about what your team will and won’t ask them to do. A simple warning can go a long way. For instance, letting cardholders know you’ll never ask them to share their bank account or card details over the phone can be the difference between a scam succeeding and failing.

3. Decide whether you want to manage fraud in-house or outsource it

Managing fraud in-house gives you full control. But it comes at a cost. High headcount, ongoing training, and constant system upkeep all add up. As you expand, your setup will also have to scale to handle higher volumes and different regional requirements.

Outsourcing can reduce that burden significantly, but working with multiple vendors across debit card and credit card fraud detection, dispute management, and card processing introduces its own complexity. If you decide to outsource, find a provider that can cover the full scope, so you’re gaining the needed capabilities and expertise without adding extra relationship and contractual complexity.

In practice, most issuers struggle to manage fraud consistently at scale. That’s where the decision between building in-house and partnering becomes critical.

What to look for in a card fraud detection solution

Understanding fraud is one thing. Implementing a system that keeps pace with it (i.e., across markets, card programmes, and regulatory frameworks) is where most issuers face friction.

If you do decide to outsource, here’s what to look for:

- Regional expertise and compliance knowledge: The right provider stays on top of regulatory requirements that affect fraud detection, such as PSD2 risk-based authentication and exemption thresholds, scheme regulations around hard and soft transaction declines, and regional variations in KYC and merchant onboarding that result in loopholes fraudsters and cybercriminals can exploit.

- Scalability: The right solution should grow with you, not just get you through the next year or two. Look for one that can handle new card programme types, expansion into new regions, and increasingly sophisticated fraud patterns without requiring an overhaul each time.

- Transparency and communication: It’s important to be aware of what rules are in place, how they’re performing, and what patterns are emerging in your portfolio. A good provider keeps you informed and maintains an open line of communication, whether that means regular hands-on collaboration or lighter-touch reporting.

- A human layer behind the technology: Technology alone is not enough. Look for a provider that can translate what’s happening in your portfolio in plain terms and collaborate with you on a fraud prevention strategy. Equally important is the flexibility and responsiveness to make rule changes quickly when needed, without lengthy back-and-forth processes slowing you down.

- Deep understanding of your portfolio: Fraud looks different across every programme. A solution that understands the specifics of your portfolio – typical transaction behaviour, cardholder demographics, local fraud trends – will be better at distinguishing genuine anomalies from normal activity.

Ultimately, the right solution should reduce operational burden while improving detection accuracy, giving you the confidence to scale without adding complexity, headcount, or risk.

How Enfuce helps card issuers detect fraud in real time and scale across markets

For issuers, fraud detection is tightly connected to authorisation, processing, dispute management, and compliance. Managing these across separate systems creates friction, delays, and blind spots.

Enfuce can help. Trusted by 60+ customers, Enfuce is a card issuing and processing platform operating across the UK, Europe, and South America. Our fully managed fraud prevention is built into the same cloud-based, API-first platform that supports your entire card lifecycle, bringing your issuing, processing, and fraud protection together in one place.

Our in-house fraud operations hub, which monitored 253M authorisations in 2025, uses Featurespace’s ARIC platform to detect and flag abnormal behaviour in real time.

The platform’s adaptive, specialist-defined rules – built on industry best practices and portfolio-specific analysis – work in combination with our machine learning-driven risk scoring. This enables our team to continuously analyse, spot new patterns, and update the rules to minimise false positives, helping your cardholders get the best possible experience.

Fraud intelligence is also shared across all our card programmes, so what we learn from one strengthens protection for all.

Enfuce’s fully managed service also covers issues that occur upstream.

When card schemes report a potential data breach, we handle Compromised Account Notifications and conduct our own Common Purchase Point (CPP) analysis to identify potential data leakage points. When a compromise is detected, Enfuce takes care of the operational response by notifying your customer service team, coordinating card replacements, and informing affected cardholders.

This approach brings you 3 key advantages for your fraud detection:

1. Stay ahead with real-time fraud detection and rapid adaptability

As fraud tactics grow more sophisticated, detection systems need to adapt just as quickly, without relying on manual updates or slow internal processes, which become liabilities. Keeping pace requires constant attention, deep expertise, and a system that moves as fast as the landscape does.

Enfuce’s 24/7 fully managed fraud operation is designed to adapt in real time. Our specialists monitor fraudulent activity around the clock, continuously analysing portfolio behaviour, tracking emerging fraud trends, and optimising detection rules, so your protection evolves as threats do. Our team then flags unusual activity to your team for further investigation via API or through our MyEnfuce portal, giving you up-to-date visibility into alerts, cases, card status, and resolution history.

You also have direct access to our fraud specialists and customer success team, so you can quickly discuss and implement rule changes quickly, without slow IT ticketing processes.

2. Get sharper detection with shared intelligence and human expertise

Enfuce supports the full spectrum of card types – from credit, debit, and prepaid to multi-PAN , open and closed loop, and industry specific solutions (e.g., fleet, EV, employee benefits, government cards) – across a single, consistent infrastructure. This allows us to detect patterns across programmes and apply those insights immediately, so we can identify emerging threats earlier, even before they impact your portfolio.

At the same time, our specialists go beyond monitoring by engaging with you directly. We meet with you regularly to review how your programme is performing, discuss whether rules need adjusting, and share the latest fraud trends relevant to your portfolio. It’s an ongoing optimisation process, not a set-and-forget service.

3. Cut costs and complexity with integrated, scalable fraud management

Building and maintaining an in-house fraud operation is expensive. Specialist hires, ongoing training, system integrations, and the operational overhead of managing disputes all add up.

With Enfuce, you can centralise fraud detection alongside card issuing and processing in one place, rather than managing them across separate systems.

For issuers that want to go further, our optional dispute management service takes the resolution process off your plate. You gather the information; we handle everything else, including chargebacks, merchants and scheme reporting, balance write-offs, and arbitration and compliance cases.

As your programme grows, Enfuce grows with you. Whether you’re entering new markets or launching new card types, we bring in regional experts to keep your programme compliant and work with you to configure fraud detection rules for each new programme.

The result is a leaner, lower-cost operation: one partner covering issuing, processing, fraud prevention, and dispute management across every product and region you operate in, without the overhead of managing multiple vendors as you scale.

How one client went from 315+ monthly disputes to a 70% reduction after migrating to Enfuce

Before migrating their credit card programme to Enfuce, one client was managing upwards of 315 disputes every month – the equivalent of more than ten every single day, with each one demanding time, resources, and resolution. Despite the volume, they had little visibility into what was driving the disputes and how to make sense of it.

That changed when they moved to Enfuce. The client now has a dedicated team to work with, full visibility into what’s driving disputes, and a clear plan to address them.

Before going live, our team worked hand-in-hand with the client to gather all available information and put tailored rules in place. This included defining what action to take when spotting suspicious activities, how much to decline, and where to set the limits.

As a result, dispute volumes dropped by over 70%, and the numbers continue to stay at a low-risk level according to industry standards.

Partner with Enfuce to protect your cardholders and your bottom line

Fraud detection is not just about stopping suspicious transactions. It’s about protecting customer trust, maintaining compliance, and enabling your card programme to scale without operational strain.

Issuers that get it right create smoother customer experiences, lower dispute volumes, and free up internal teams to focus on growth.

Enfuce brings fraud prevention, dispute management, issuing, and processing together in a single platform, giving you the visibility, control, and expertise needed to manage fraud without added complexity.

Whether you’re scaling into new markets or optimising an existing programme, we’re ready to help. Contact us today.

FAQs about card fraud detection

What is real-time card fraud detection, and why does it matter?

Real-time fraud detection means monitoring every card transaction and flagging suspicious activity as it happens. It matters because fraud moves fast. If your system isn’t analysing behaviour in real time, fraudulent transactions slip through before you can stop them, driving up dispute volumes and damaging the cardholder experience.

What should I look for in a card fraud detection solution?

Look for a provider with regional compliance expertise, scalability across card programme types and geographies, and a strong human layer behind the technology. Transparency and communication matter too, as does a deep understanding of your specific portfolio. Also, the more card programmes and regions a provider covers, the richer their fraud intelligence and the better their ability to catch emerging threats early.

Do card-issuing platforms offer fraud detection?

Some do, and it’s worth looking for one that does. When fraud detection is built into the same platform handling your card issuing and processing, you avoid the complexity of managing multiple vendors and integrations.

With Enfuce, fraud prevention and dispute management are part of the same modular platform as card issuing and processing, meaning you get full coverage from a single partner without the fragmentation of a multi-provider setup.

Let’s talk.