Virtual card issuing: How to pick the right platform

For businesses looking to issue virtual cards, getting started isn’t always straightforward. What works for an expense management platform may not suit a fleet operator or an employee benefit provider.

That leaves product and innovation teams balancing competing demands from day one: delivering a seamless customer experience while meeting regulatory requirements, controlling costs, and building a programme that can scale across markets and use cases.

This means virtual card issuing is unique, shaped by your particular use cases and constraints. It requires careful trade-offs between flexibility, control, and compliance from the outset.

This raises lots of questions:

- Should you focus on single-use cards for security?

- Enable cards for digital wallets through tokenisation?

- Support a hybrid experience for customers who still expect plastic alongside digital?

The right answer depends on how your card programme is designed and who it’s built for. That’s why choosing the right issuing and processing platform matters. The provider behind your programme needs to support multiple card types, use cases, and markets without adding unnecessary complexity as you scale.

As a secure, compliant card issuing and processing platform, Enfuce has spent over a decade helping businesses design and scale virtual card programmes across financial services, fintech, expense management, employee benefits, and fleet and mobility. In this guide, we’ve brought that experience together into the key considerations you need to get virtual card issuing right.

Read on to find out:

- What you can do with virtual cards

- How to issue virtual cards

- What to look for in a virtual card issuer or platform

- Why choose Enfuce as your virtual card issuing platform

- How Enfuce helped Swile launch an all-in-one employee benefit card for millions of users

- FAQs

Looking for a flexible virtual card issuer? Enfuce is a global card issuer and processing platform that can help. Reach out today to learn more

What you can do with virtual cards

Before diving into what virtual cards make possible, it’s worth clearing up some terminology.

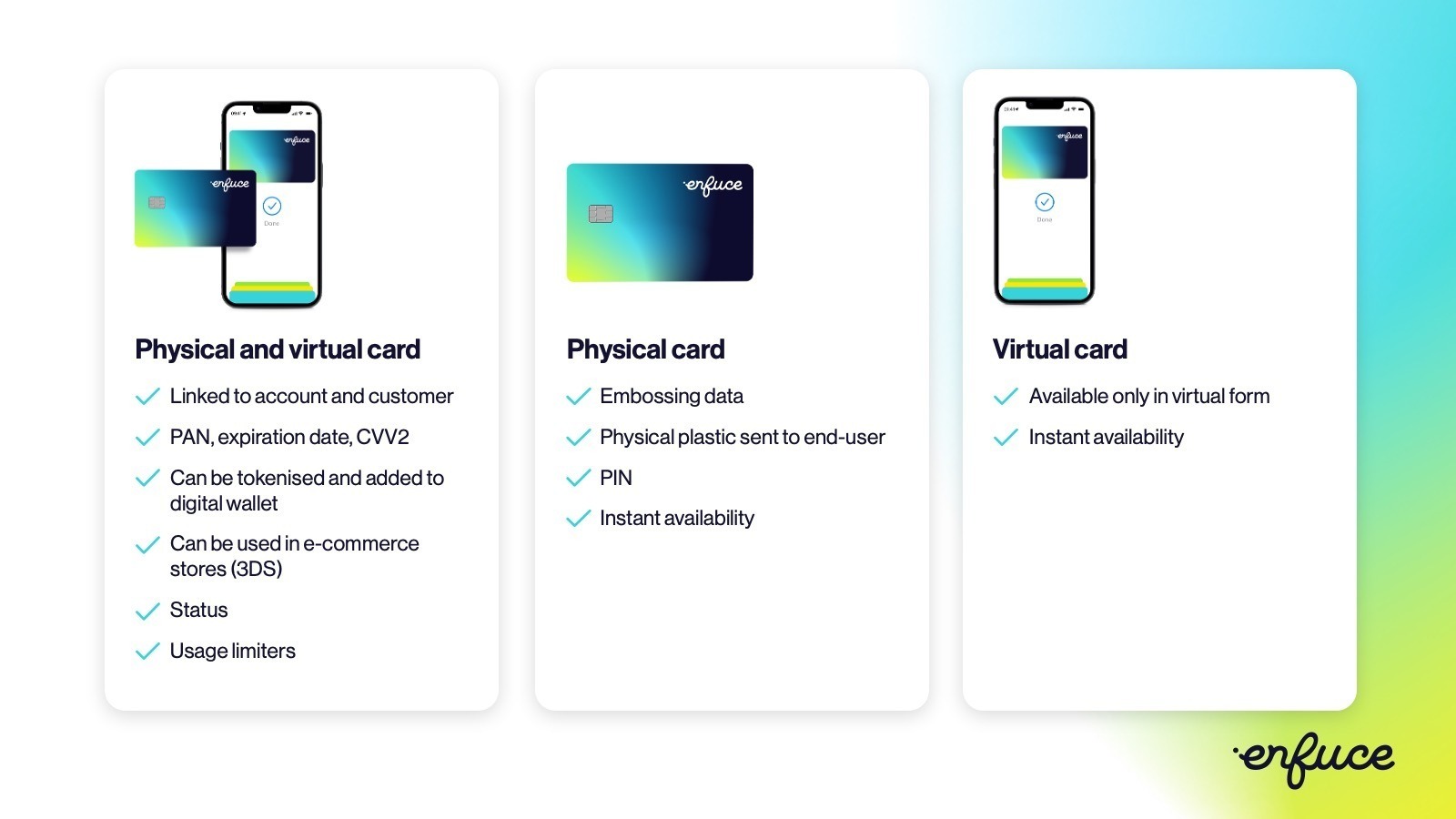

Virtual cards are digital payment methods. They have all the details you’d expect – a card number, CVV, and expiration date – but, unlike physical payment cards, these details exist digitally rather than printed on a piece of plastic.

Virtual card issuing can vary:

- Some virtual cards are virtual-only, meaning no physical counterpart is issued.

- Others can have a physical equivalent issued alongside them down the line if the cardholder’s preferences change.

- A single card can be issued in both physical and virtual forms at the same time.

This means deciding between physical and virtual cards isn’t always an either/or decision for issuers.

With that settled, let’s look at what you can do with virtual cards.

What are the benefits of virtual card issuing?

Compared to physical cards, virtual cards can offer greater speed, control, and security across the entire card lifecycle.

First, they’re faster to issue and immediately usable. Virtual cards can be created on demand and used straight away for online payments or added to digital wallets, allowing cardholders to start spending without delay. A neobank, for instance, can issue a virtual card to get a new customer spending on day one.

You can even instantly issue virtual versions of physical cards that can be added to digital wallets immediately.

This way, if physical cards are your main value proposition, that additional virtual offering can enhance your customer’s experience, allowing them to start using their card right away.

Virtual cards can also be issued for a specific purpose or time period and closed just as quickly, without any physical card remaining in circulation.

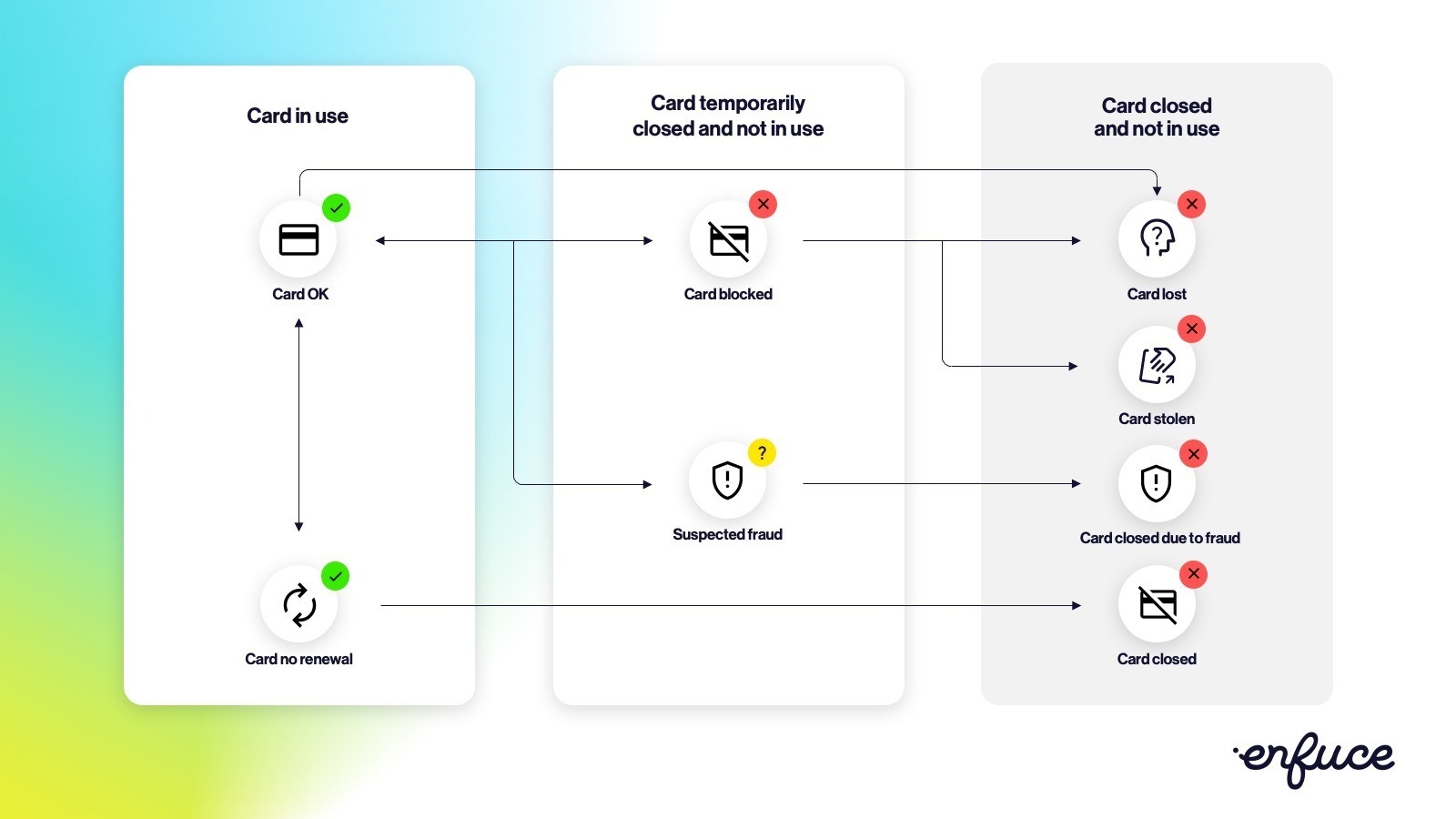

With no printing, personalisation, physical PIN handling, or mailing involved virtual cards are also more affordable to produce. And because you can issue and close them instantly, issuers have full control over the entire card lifecycle.

An example of managing the entire card lifecycle, whether virtual or physical

What are the various use cases for issuing virtual cards?

Virtual cards enable use cases that aren’t practical with plastic and are highly dependent on the industry. Here are a few examples across different sectors:

- Expense and spend management: Businesses can issue virtual prepaid or corporate cards to employees for business-related purchases, get greater control and visibility over spending and cash flow, and automate expense reconciliation. Businesses can also issue dedicated virtual cards tied to specific recurring subscriptions instead of a staff member, so if an employee leaves, payments don’t get disrupted.

- Employee benefits: Benefit platforms can issue virtual cards that support specific benefit categories such as meals, mobility or wellbeing, or combine multiple benefit applications through multi-PAN setup where relevant. These cards can be added to the digital wallets, giving employees a simple way to access benefits in everyday situations.

- Fleet and mobility: Fleet operators and mobility platforms can issue virtual cards configured for fuel and mobility-related charges and deliver them directly to drivers’ digital wallets. With real-time spend visibility and merchant category controls (MCC), they can monitor usage as it happens and restrict spending to approved categories, improving both oversight and cost control.

- Non-profits and governments: Virtual cards offer a fast, auditable way to distribute funds for specific programmes or projects. You can restrict spending to approved categories from the moment of issuance, making reconciliation straightforward and creating a clear paper trail.

- Gift cards and incentives: Businesses can issue prepaid virtual gift cards with short validity periods, making them fast and cost-effective to distribute for promotions, rewards, or one-off payouts.

- Financial services and neobanks: A neobank or financial services provider can launch card programmes faster by issuing virtual cards to new customers from day one and enabling spending immediately.

The examples above only scratch the surface. Virtual cards are still an evolving space, and businesses across industries are finding new ways to use them as payment solutions. But whatever your vision, the starting point is the same: understanding how issuance works.

How to issue virtual cards

How you issue virtual cards depends on your setup. If you’re working with an API-first issuing platform like Enfuce, here’s what the process looks like:

- Customer data collection and onboarding: You, the issuer, are responsible for collecting and managing customer information and handling onboarding. Once complete, the customer and account are created in Enfuce’s system. Cards must be linked to both, so this step is the foundation for everything that follows.

- Create card via API: Your application sends a card creation request to Enfuce’s API, including key details such as whether the card should be virtual or physical. For virtual cards, you can choose between:

- Virtual-only cards: These cards are permanently virtual, with no option to issue a physical equivalent.

- Digital cards: You choose at issuance whether to issue a physical card or keep it virtual. This decision doesn’t have to be final. Enfuce’s Update Card API lets you change it later, even after the card has been issued.

- Card setup: When the request is processed, the card is created and associated with the customer and account. Your predefined product settings, such as spending controls, transaction permissions, fees and validity period, are applied automatically.

- Virtual (and physical) cards are usable immediately after issuance: Virtual card details are immediately accessible for e-commerce transactions, and cards can be enrolled into mobile wallets like Apple Pay or Google Pay after card onboarding. To support digital wallets, you must integrate with the relevant scheme tokenisation and authentication services, which Enfuce’s Digital Wallet module can manage for you.

- Manage cardholder controls: With Enfuce’s APIs, you can embed card management in-app or on your website and let cardholders view card details, set and view their PIN, reorder cards, and more.

Of course, this is just one way the process can work. Ultimately, the issuing infrastructure you choose determines how smooth each of these steps actually is.

What to look for in a virtual card issuer or platform

The platform you choose should be flexible enough to support your business model, customer base, and growth plans. Here’s what to prioritise when evaluating a virtual card issuing platform:

- API-first architecture: An API-first approach means faster implementation, greater flexibility, and the ability to embed card functionality directly into your own product.

- Cardholder UX capabilities: As the issuer, you own the interface your cardholders interact with, but you’ll depend on your issuing platform to power it. Make sure the APIs support the experiences cardholders expect: viewing card details, setting and checking PINs, reviewing card transactions, requesting physical cards, and more.

- Physical and virtual flexibility: Avoid getting locked into one card format. Look for a partner that supports virtual-only cards, physical cards, and digital cards with an optional physical equivalent, so you can meet your cardholders’ evolving preferences and adapt your programme over time.

- Multiple card types: Beyond format, consider whether the platform supports the card types you may need – prepaid, debit, and credit – and the networks you want (i.e., Visa, Mastercard) as well as more specialised programmes like fleet cards and gift cards. Be sure to think ahead to the card types you might need as your strategy evolves.

- Multi-country support: If expansion is on your roadmap, your issuing platform should be able to grow with you by fast onboarding and handling local BINs and regulatory requirements without requiring a separate provider.

- Migration support: If you’re already working with an issuer, look for a provider that offers dedicated migration assistance to minimise disruption to your programme and your cardholders.

Ultimately, the right platform meets your programme where it is today and grows with it from there. That means one issuing and processing partner covering your use cases, markets, and card formats, not a patchwork of providers stitched together as your strategy evolves.

Why choose Enfuce as your virtual card issuing platform

Enfuce is a secure, compliant card issuing and processing platform operating in Europe, the UK, and South America.

Our modular, API-first infrastructure gives you the flexibility to build your card programme your way. We provide the infrastructure, scheme access, and compliance guardrails, while you define your customer journey, product features, and the experience your cardholders get – including how and when virtual cards fit into the picture.

Here’s what you can expect with Enfuce as your issuer processor:

Meet cardholder preferences with virtual and physical card issuing

Virtual cards are growing, but they haven’t replaced physical cards entirely. Some cardholders will go fully virtual, others will want digital convenience with a physical backup, and some aren’t ready to move away from plastic at all. So, as an issuer, how do you build a programme that doesn’t lock you or your cardholders into a single format?

With Enfuce, you can issue both physical and virtual cards. Virtual cards are immediately usable for online and offline payments from the moment they’re issued. And physical cards – while printed and shipped – can be added to digital wallets like Apple Pay and Google Pay as part of the initial signup flow, making them instantly spendable before the plastic arrives.

What sets Enfuce apart as a virtual card issuer is our “phygital” option. Rather than locking cardholders into a single format at onboarding, our Digital Card feature lets your customers choose at any point in their lifecycle whether they want a physical card or remain fully virtual, with the flexibility to change that decision over time.

Because virtual and physical card formats can be managed within the same Enfuce card programme, you don’t need to run entirely separate programmes to support both experiences. It’s a straightforward way to deliver an omnichannel payment experience and show your cardholders their preferences are built into your product, not treated as an afterthought.

With Enfuce, you can also offer virtual disposable cards, combine multiple card applications (i.e., multi-PANs) into one card, and combine a debit and credit card into one card, as seen in Swile’s dual-PAN setup for employee benefits.

These are just a few examples of how our platform enables your strategy rather than constrains it.

From day one, our expert teams work with you to identify the use cases that make the most sense for your programme and your customers. Then we help you design and implement them. Whether you’re launching a new programme or evolving an existing one, we bring the experience to help you issue the right cards.

Want to explore our capabilities? Developers can create an account in our customer portal, MyEnfuce, and explore our APIs in a dedicated sandbox environment.

Simplify virtual card management with an API-first, cardholder-first CX

One of the biggest advantages of virtual cards is how easy and cost-effective they are to create. But the more virtual cards a cardholder has, the more important it is to give them a clear, centralised way to manage them all. Without the right customer experience (CX), what starts as a convenience can quickly become a source of headaches.

Enfuce’s API-first approach makes it easy to embed card issuing and management directly into your existing systems. Rather than redirecting users elsewhere, you can give them a white-labelled and branded experience within your own desktop or mobile application.

Card management includes secure access to key card details and PIN management. Cardholders can set their own PIN, check it whenever they need to, and change it at ATMs if they prefer. And because Enfuce handles sensitive card data on your behalf, you can build these features into your application without taking on the burden of PCI compliance yourself.

Your cardholders can also freeze, geo-block, cancel, and reorder cards themselves. These features give them greater control, especially in time-sensitive situations when a card has been lost or stolen.

Altogether, Enfuce makes it straightforward to deliver a card management experience that feels native to your product, puts cardholders in control, and keeps the operational burden off your team.

Scale to multiple markets with a flexible, future-proof issuing platform

New opportunities don’t always fit neatly into your existing setup. A new market brings its own regulatory requirements, currencies, and customer expectations, while a new product line might call for an entirely different card type or programme structure.

With Enfuce, you get a comprehensive card issuing platform designed for multi-market scalability.

Multi-country support is available from the start. That includes local BIN support, scheme and invoicing requirements, and KYC/KYB and customer activation flows aligned to the regulatory requirements of each market. Reporting is localised, giving stakeholders the reconciliation, compliance, and operational data they need in the format they expect.

Enfuce also supports prepaid cards, debit cards, and credit cards across virtual, physical, and digital formats. These can be applied across consumer, commercial, and B2B use cases, including specialised cases like gift cards and fleet and fuel cards. And because our platform is modular, you only pay for what you use. Launch with what you need today, and layer in complexity as your strategy evolves, without having to migrate to a new platform every time your requirements change.

How Swile launched an all-in-one employee benefit card for millions of users with Enfuce

Swile is a French platform transforming how employee benefits are paid out and used, with over five million cardholders and 100,000 corporate customers across Europe and Latin America.

Swile wanted to improve the employee benefit experience with a single card that could support multiple benefit categories, from meal benefits to mobility and culture-related spending. The challenge? Each benefit type carries its own rules, tax treatment, and spend restrictions.

That meant Swile needed an issuer processor that could handle multiple PANs, scheme-specific rules, and dynamic benefit settlement, ensuring transactions are correctly allocated across different benefit categories. They also wanted a partner that could keep up with its plans to build innovative employee experiences. Enfuce delivered on both.

Together, Swile and Enfuce built a next-generation card usable in-store, online, and via digital wallets, with granular spend controls that let customers define when, where, and how the card can be used. Behind the scenes, Enfuce’s technology handles full compliance with benefit regulations and supports robust reporting capabilities.

The card launched successfully across Western Europe, laying the groundwork for Swile’s expansion into Brazil, where they launched dual-PAN cards for over one million Brazilians.

Quentin Vigneau, Product Director of Payments at Swile, described the partnership: “This collaboration is instrumental in our ability to move fast across multiple geographies with an iterative approach to innovate. I guess it’s really about this great feeling you get with outstanding partner teams: they seem to be fully part of the company.”

Find out more about how Enfuce helped Swile revolutionise employee experience management.

Start issuing virtual cards with Enfuce

Launching a new card programme or evolving an existing one both come with the same underlying challenge: choosing a platform that can keep up with the evolving demands of your customers and growth plans.

Enfuce gives you the modular, API-first infrastructure to build a programme that works for your cardholders today and scales with you over time, whether that means virtual cards, physical cards, or both.

Ready to get started? Contact us today to talk through your virtual card strategy.

Frequently asked questions about virtual card issuing

What is a virtual card?

A virtual card is a digital payment card. It has all the details you’d expect – a virtual card number, CVV, and expiration date – but the difference is that these details exist digitally rather than printed on a piece of plastic. Some virtual cards are virtual-only, meaning no physical counterpart can ever be issued. Others can have a physical equivalent issued alongside them or down the line if the cardholder’s preferences change.

Who can issue virtual cards?

Virtual cards can be useful to almost any business, but issuing them in-house means building your own infrastructure, obtaining the right licences, and securing scheme memberships, which is a significant undertaking. In practice, businesses across industries typically partner with a virtual card platform or issuer to handle that complexity.

What is a virtual card issuing platform?

A virtual card issuing platform enables businesses to create and manage card programmes, including card issuance, transaction authorisation, and lifecycle management.

Many platforms support a range of card formats and use cases, from virtual-only cards to combined physical and digital experiences. Enfuce brings issuing and processing together on one platform, giving businesses the flexibility to support multiple card types and evolve their programme over time.

What are the most common use cases for virtual cards?

Virtual cards are highly versatile, with use cases that vary widely across industries. For example, in expense management, businesses can instantly issue cards for employees or even specific subscriptions, giving them tighter control and real-time visibility over spending. In financial services, virtual cards let new customers start spending immediately.

Virtual cards can also be time-bound or limited to certain categories, which can help cut down on misuse and admin work in industries like employee benefits.

Let’s talk.