Card businesses are data-rich and insight-poor. Here’s how Embedded Analytics changes that.

As a card programme operator, you already have access to huge volumes of data. Every authorisation, transaction and fraud signal generates operational insight.

But the challenge isn’t access to data itself. It’s turning fragmented, fast-moving information into something teams can actually use to make decisions.

And the world of analytics has also moved on, shifting toward real-time, AI-driven decision support while many card businesses remain stuck in the overhead of operational analytics itself.

Analytics infrastructure becomes a parallel product that needs to be built, maintained, secured, governed, and continuously updated. Reporting logic evolves. New compliance requirements emerge. And internal teams wind up spending more time managing pipelines and dashboards than extracting actionable insight from them.

That creates a familiar problem across issuing and processing: card businesses become data-rich, but insight-poor.

As a cloud-native issuer processor and dual-licensed EMI supporting card programmes across Europe and the UK, Enfuce operates large-scale data infrastructure every day across issuing, processing, fraud monitoring, ledgering, and programme management.

We developed Embedded Analytics from that operational reality: giving card businesses direct access to ready-to-use analytics, without the overhead of building and maintaining the infrastructure themselves.

In this article, we share what led to Embedded Analytics, covering:

- The analytics landscape today (and where most card businesses are stuck)

- What’s making it hard for card businesses to move forward

- Why Enfuce was well-positioned to solve the analytics challenge

- How Embedded Analytics gives customers ready-to-use analytics

Interested in ready-to-use analytics for your card programme? Reach out to Enfuce.

The analytics landscape today (and where most card businesses are stuck)

Turning available data into usable insights has become one of the hardest problems in card issuing and processing.

Card programmes generate continuous streams of information across authorisations, fraud events, spending behaviour, repayment activity, and customer usage patterns. In theory, that should make decision-making easier because the potential insights are significant:

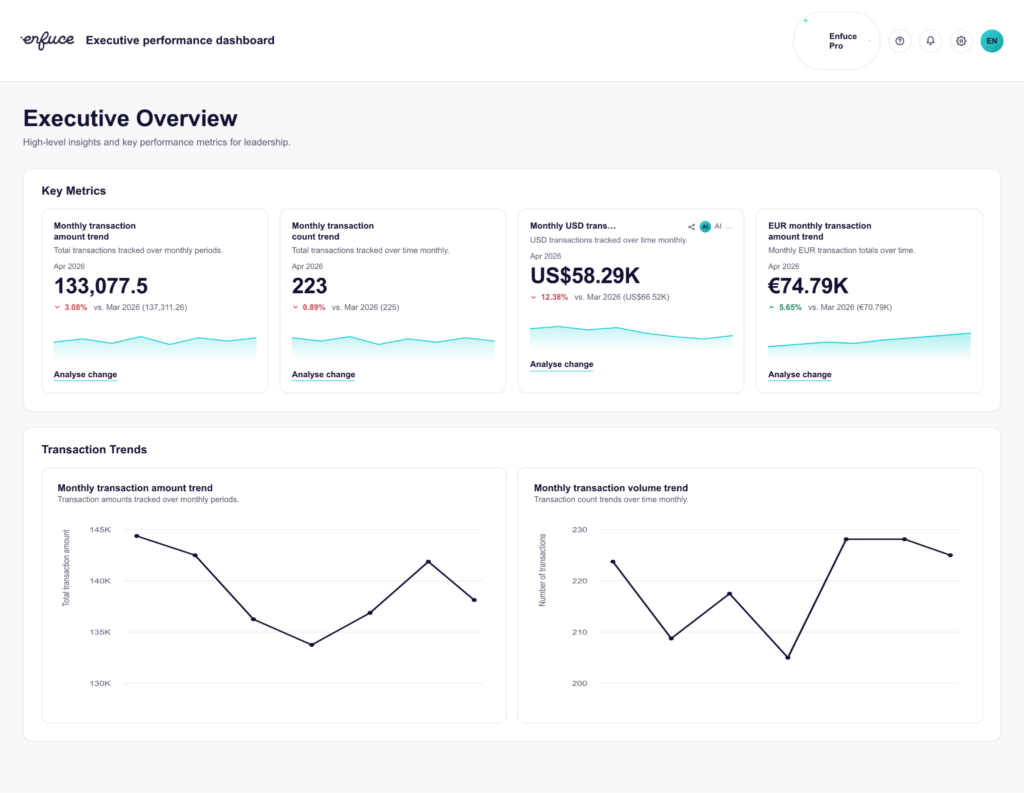

- Finance teams could be tracking portfolio health and repayment behaviour in real time, not at the end of the month

- Fraud and risk teams could be spotting patterns before they become incidents, not after

- Programme managers could see exactly which cards are being used, where activation is stalling, and where revenue is leaking

- Strategy managers could be benchmarking performance against peers and identifying expansion opportunities supported by market insights

In reality, many teams still struggle to surface insights quickly enough to influence operations, risk, or growth. The problem is industry-wide: most analytics setups were never designed for the fragmented reality of card operations, where data is spread across multiple systems, teams, and reporting layers.

Over time, analytics as a discipline has moved through three broad phases:

- The dashboard factory: A centralised data team owns every report, dashboard, and query. Operational teams file requests and wait – sometimes weeks – for answers. Decisions move at the speed of the queue.

- Self-service business intelligence (BI) solutions: Tools like Tableau and Power BI put data directly in the hands of operational teams. The bottleneck doesn’t disappear, but moves. Each team now has to define its own metrics, interpret its own data, and maintain its own dashboards, without the analytical training needed to do it well.

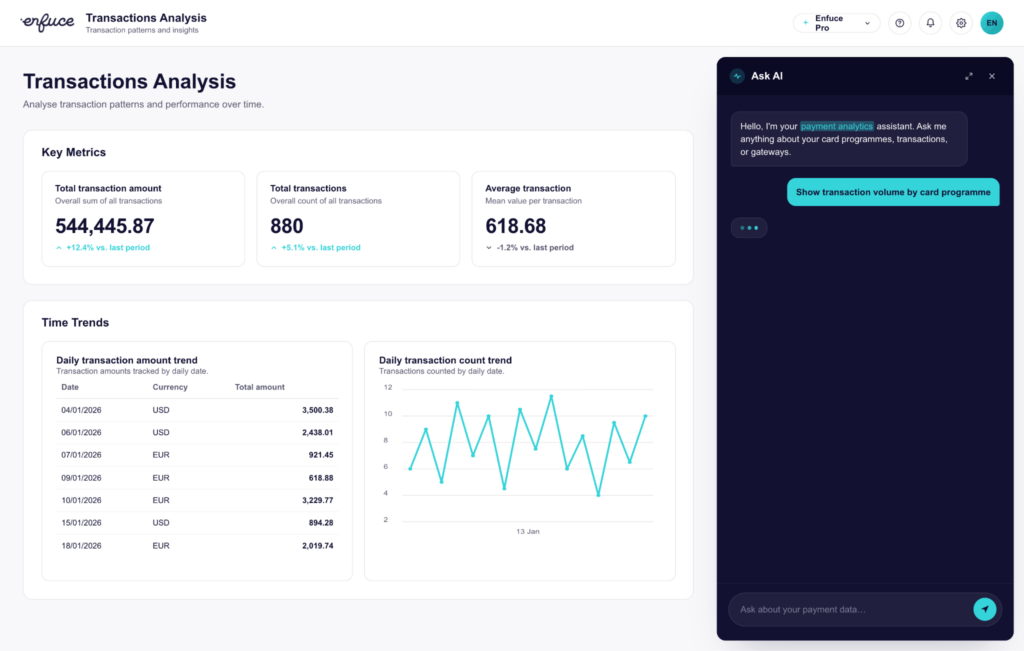

- Conversational, AI-driven analytics: Teams ask questions in natural language and get answers in seconds. No dashboard to build. No metrics to define. No SQL to write. Analytics finally stops being a workflow and starts becoming a conversation.

Most card businesses are still operating between phases one and two. In both cases, the underlying problem is similar: the infrastructure needed to turn data into decisions can’t keep up with the decisions that actually need to be made.

Either way, decisions don’t get faster. They get harder to make.

Analytics either moves at the pace of overloaded central teams, or it shifts complexity onto operational users who weren’t hired to manage data tooling. The third phase, the one where analytics actually drives faster, smarter decisions, stays out of reach. Let’s look at why.

What’s making it hard for card businesses to move forward

Whether you’re building analytics from scratch or trying to scale what you already have, the obstacles that keep businesses in the early phases tend to fall into three categories.

1. The build cost is high in time, money, and ongoing overhead

For firms starting from scratch, building a usable analytics foundation means investing in data warehousing, BI tooling, integrations, governance, and specialist hires – easily costing over €200K per year before a single insight is delivered. Then add months of implementation work before operational teams can rely on the output.

For firms that already have internal analytics capabilities, the challenge is maintenance.

Custom models, dashboards, and governance frameworks all require ongoing upkeep as card programmes evolve. A new card product, changes to fraud monitoring requirements, expansion into new markets, scheme reporting updates, or requests for different portfolio views from finance and risk teams can all trigger additional analytics work.

Analytics teams end up spending more time maintaining the analytics function – data pipelines, reporting logic, and dashboard definitions – than helping the business move faster.

2. Card data is complex, with different teams demanding specific insights

The questions different teams ask vary significantly. What a finance lead needs for a portfolio health report differs from what a programme manager needs to track activation.

For centralised data teams, this creates a scope problem. Fielding requests across finance, risk, product, and commercial functions means constantly context-switching between different business questions, definitions, and outputs, often without the domain knowledge to know whether the answer is actually useful for that decision.

A fraud team investigating unusual authorisation behaviour, for example, needs a very different level of granularity and context than a commercial team reviewing programme growth across markets.

Giving teams more direct access to data doesn’t always resolve it either.

Domain expertise and analytics expertise rarely sit in the same person.

A product manager may understand exactly why virtual card activation is declining in one customer segment, but not know how to query the data to validate that hypothesis. Analytics teams may be able to query the data, but lack the operational context to interpret what matters.

The gap only closes when someone, or something, can do both.

3. Card analytics teams can’t keep up with demand

Even mature analytics teams can hit a ceiling. Every new question that needs answering typically requires new data work: building a new dashboard for portfolio segmentation, adjusting reporting logic for a new market, modelling fraud trends differently, or creating new views for finance or compliance teams. That work then competes with ongoing maintenance, governance, and reporting requests already in progress.

The result is a growing gap between the operational questions your teams need answered and what your analytics function can realistically deliver at the required speed. In the meantime, people are forced to make decisions on incomplete information:

- Fraud teams don’t see emerging transaction patterns early enough

- Programme managers can’t identify where activation rates are dropping

- Commercial teams lack a consistent view of programme performance across markets

This keeps organisations operating reactively within the first two analytics models: either relying on central teams to fulfil reporting requests or pushing analytical responsibility onto operational users themselves.

And the third phase – conversational, AI-driven analytics, where teams surface insights, identify anomalies, and support decisions in real time – stays out of reach. Not because the technology isn’t ready. But because your data team is too busy maintaining their existing analytics to build what comes next.

Why Enfuce was well-positioned to solve the analytics challenge

Embedded Analytics didn’t start as a product initiative. It started as a problem we had to solve for ourselves internally.

Enfuce is an EMI, BIN sponsor, and issuer processor. We process transaction data every day across multiple markets, schemes, customer segments, and card programmes. To operate effectively at that scale, from managing fraud and reconciling finances to supporting customers and identifying growth opportunities, we needed deep visibility into our own data.

To support that, we developed internal analytics capabilities used across operational, risk, finance, and commercial functions. Our teams used analytics to monitor card-programme performance, analyse transaction behaviour, track fraud patterns and false positives, support reconciliation and credit-control workflows, benchmark performance across markets, and generate operational, sales, and customer-success insights. For years, this was just how we worked.

This created deep expertise both in managing card data infrastructure and understanding what payments data actually reveals when modelled and analysed properly.

Over time, we kept hearing the same challenges from our customers. They wanted the same level of insight into their own programmes. Not raw data, but the analytics we’d already built.

We chose to build a managed analytics capability, not raw data exports or another self-service toolkit, but something built directly on top of the transaction and operational data we were already processing for our customers.

What shaped the specifics came largely from deep client insights. One fleet operator, for example, wanted to combine accounts receivable and credit reconciliation into a single operational view integrated directly into their accounting systems. Similar requirements emerged across different customers, operational models, and verticals, gradually defining the analytics capability we set out to build.

Embedded Analytics is the result of that process.

How Embedded Analytics gives customers ready-to-use analytics

Embedded Analytics is a managed analytics service built on Enfuce’s source-of-truth payments data and delivered through myEnfuce customer portal.

We designed the service around two aspects: the kinds of operational challenges card programmes need to solve, from transaction monitoring and fraud analysis to portfolio reporting and commercial benchmarking, and the different ways teams want to work with analytics, from ready-made dashboards to conversational AI.

To support that, Embedded Analytics combines:

- Different capability levels, depending on how independently your teams want to work with data

- Domain-specific analytics products designed around operational, financial, risk, and strategic use cases

Here’s how that works in practice:

1. Get programme insights in weeks without the infrastructure burden

For teams starting from scratch, Embedded Analytics removes the build entirely. No data warehouse to procure, no BI layer to configure, no specialist team to hire, no months of waiting before insights are usable.

For teams that have already invested in internal analytics, it removes the maintenance burden. Models, dashboards, and governance are all managed by Enfuce and updated as your programme evolves.

Our model is flexible, with different Capability Tiers. The three tiers map to the three eras of analytics we described earlier, and they’re designed so customers can start where they are and grow into the next era without changing platform:

- Explorer: For teams that want reliable analytics out of the box, this tier offers pre-built dashboards with data you can filter, drill down, and run ad hoc searches on. Best for fast data exploration, reporting, and analytics.

- Builder: This tier gives you more ownership over your data, letting you create and share custom dashboards, manage insights, and access underlying datasets without building your own infrastructure. Best for frequent data users looking to eliminate the reporting bottleneck.

- Analytics Agents: For teams ready to scale data-driven decisions, this tier lets you ask questions in natural language and generate insights automatically with AI. Best for those who want advanced analytics but not the complexity of building it.

Whichever tier you choose, our established capabilities mean your team can start working with reliable analytics within weeks, not months.

2. Deliver trusted, usable analytics across every team in your business

Different functions need card data to answer different questions. A finance lead investigating overdue balances has nothing in common with a fraud analyst tracking decline patterns, except that they both need answers, fast.

Embedded Analytics gives them packaged analytics products, not raw datasets. Each one is designed around a specific business problem, with domain expertise built in.

Our domain-specific Analytics Products are grouped into three categories. The products span an arc from operational control to strategic growth, from the day-to-day questions every card programme needs to answer, to the strategic decisions that shape where the business goes next:

- Core Analytics covers the fundamentals every card programme needs, including transaction insights, authorisation declines, and cardholder segmentation.

- Operational Analytics goes deeper for teams making day-to-day operational decisions, covering fraud intelligence, credit portfolio and invoicing, financial analytics and reconciliation, and regulatory reporting.

- Strategic Analytics draws on Enfuce’s data across countries, merchants, and verticals to give a broader comparative view. Products include benchmarking, go-to-market insights, cardholder churn prevention, and cardholder upsell signals.

Because everyone works from the same source-of-truth, data, finance, risk, operations and commercial teams stop arguing about whose numbers are right and start making decisions faster.

3. Scale your analytics without growing your team

As your programme grows and questions become more complex, Embedded Analytics scales with you. Additional Analytics Products can be added as new business problems emerge, and you can move up Capability Tiers as your capabilities mature. Nothing needs to be rebuilt, everything runs on the same platform.

And because Enfuce maintains the service, updating models, expanding analytics products, and developing new AI capabilities, your team can focus on growth, innovation, and programme development instead.

The shift toward more advanced analytics doesn’t need to happen through a separate infrastructure programme. It can evolve progressively from reporting and dashboards toward AI-supported decision-making on top of the same operational foundation.

Embedded Analytics: Turning card data into operational insight

Card programmes are sitting on some of the richest operational data. Unfortunately, most of it goes underused, not because teams aren’t aware of its value, but because turning it into insight requires immense amounts of time, resources, and infrastructure.

Embedded Analytics changes that.

Built directly on top of Enfuce’s issuing and processing infrastructure, Embedded Analytics gives you ready-to-use, domain-specific analytics without the burden of building and maintaining the foundation yourself.

Your analytics function stops being something you build and maintain. It becomes something you use to make faster, better-informed decisions.