Open-loop card payment system: How to implement one (with 6 examples)

If you’re looking for an open-loop card payment system, you might be a:

- Fintech wanting to offer a single card for multiple use cases (e.g., corporate expenses) without having to rely on several providers

- Fuel or fleet operator running a closed-loop programme and wanting to expand to new markets, enter new customer segments (e.g. from heavy commercial transport into light fleets), or broaden acceptance to include EV charging, tolls, parking and more

- EV charging or mobility operator needing wider acceptance than any single network can provide

Across all of these cases, the challenge is not acceptance alone, but how to introduce open-loop payments without losing control, data quality or regulatory confidence.

In this article, we’ll share our first-hand knowledge on when closed vs open loop systems make sense and how they work. We include various use cases and how you can get started safely and compliantly through a single provider like Enfuce.

In this article:

- Open-loop vs closed-loop card payment systems: What’s the difference?

- 6 top use cases for open-loop systems (and when to use them)

- Why partner with Enfuce to enable an open-loop card system

- How OKQ8 replaced legacy card platforms and launched a scalable Visa programme with Enfuce

- FAQs

Looking to migrate to an open-loop card payment system, launch an open-network programme or take a hybrid approach? Enfuce can help —learn how by getting in touch today.

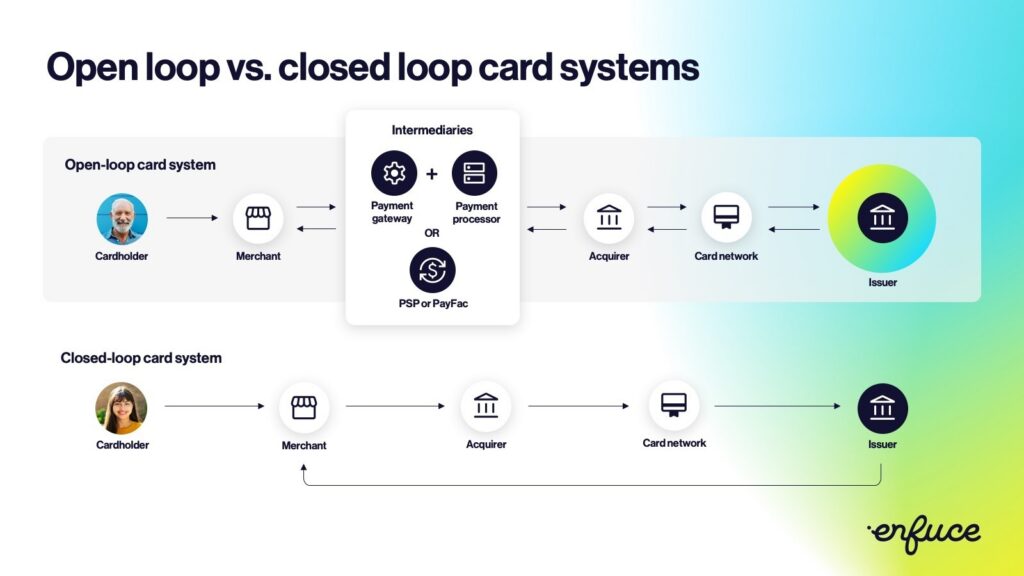

Open-loop vs. closed-loop payment system: What’s the difference?

The difference comes down to acceptance and governance:

- Closed loop is issuer-led. Acceptance is limited to a single merchant or a defined network, and rules are enforced within that private ecosystem.

- Open loop is scheme-led. Acceptance follows Visa or Mastercard rules, enabling cardholders to pay at any merchant that accepts the scheme – domestically and internationally.

We take a closer look at each below.

What is a closed-loop payment system and how does it work?

A closed-loop payment system is a card or account that is restricted to a single merchant or a specific network of merchants, such as a gift card for a specific company. In a closed loop, the issuer defines where and how the card can be used, without relying on an external card scheme such as Visa or Mastercard. In some models, the issuer is also the retailer, which makes strict controls easier to enforce.

Examples of these self-contained systems include traditional fuel cards, RFID-based EV charge cards, transit cards, retail-branded mobility cards and retailer-specific payment apps (e.g., Starbucks) or gift cards (e.g., Apple, Amazon).

For instance, say a fleet operator gives drivers a fuel card that is only accepted at a defined set of partner stations (e.g., certain Carrefour-branded sites and other contracted locations). The fuel card has certain controls in place, such as product restrictions (diesel only), geo limitations, and merchant category code (MCC) rules, so the card can’t be used outside the agreed network or permitted spend categories.

Once a driver makes a purchase, the transaction stays within the fleet operator’s private network. They often use proprietary technology to manage the funds, avoiding external card networks or intermediaries.

What is an open-loop payment system and how does it work?

An open loop is a scheme-led model (e.g., using Visa or Mastercard®) where issuers and merchants follow the scheme rules. This allows the cardholder to pay at any merchant, both domestically and internationally, that accepts the scheme.

The different types of open-loop systems can range from fleet-specific cards like Visa Fleet 2.0, corporate mobility cards, and digital wallets to expense cards and employee benefit programmes.

For example, a multinational travel company issues a Mastercard to each of its senior managers worldwide. Managers use the card to make business-related purchases (meals, accommodation, flights), anywhere that accepts Mastercard.

Open-loop card payment systems involve multiple parties (i.e., issuers, acquirers, processors, networks, and merchants), enabling transactions to be accepted broadly and settled reliably across institutions.

Open-loop issuers can usually apply controls at the merchant or category level (e.g., MCC-based rules such as “restaurants and hotels only”). Item-level restrictions (e.g., “diesel only”) generally require enhanced transaction data and supporting capabilities from the merchant/acquirer.

For example, industry programmes such as Visa Fleet 2.0 are designed to improve fleet-specific data and controls, provided the merchants and issuers support those features end-to-end.

Advantages and disadvantages of closed-loop systems

Traditionally, closed-loop cards were adopted because they enabled a level of control (item or category level) and invoicing that open card schemes did not support at the time, particularly for fleet and fuel use cases.

Advantages of a closed-loop payment system that distinguish it from open loop include:

- Tighter cost controls on where and what to spend. For example, fleet operators can restrict spending to specific locations or services to prevent misuse of fuel cards. And with data passing through a limited number of parties, it’s easier to reduce fraud because rules like approved merchants or services can be applied at the point of authorisation and exceptions are easier to spot and act on.

- Simplified VAT invoicing and reconciliation. Closed-loop programmes can issue a single consolidated VAT invoice covering all card transactions, removing the need for drivers or employees to collect and submit individual POS receipts.

- Better pricing and loyalty benefits for customers. Companies can offer discounts and rebates within their own network to improve end-customer satisfaction and retention. While it’s also possible to provide these benefits with open loop, closed-loop cards make it easier as they can set them flexibly per customer.

- Transaction fees can be lower than open loop because there are fewer third-party vendors involved (i.e., no external card networks).

Caption: the networks of open and closed-loop card payment systems

But closed loops also have their drawbacks when compared to open loops:

- Limited acceptance can be a feature or a constraint. Closed-loop cards restrict spend to a defined merchant network, which can be desirable for issuers looking to drive volume through their own retail sites, or for customers who want to enforce use of locations with the best commercial terms. In other cases, however, the same restriction is experienced as a limitation, particularly when drivers or fleets need broader geographic coverage or flexibility, reducing usage and satisfaction.

- Poor customer experience. For example, an employee may need multiple expense cards for each expense type, such as meals, fuel and accommodation. This increases frustration, unintentional misuse and admin inefficiencies.

- Regulatory and compliance constraints as programmes scale. Regulations like the EU’s Alternative Fuels Infrastructure Regulation (AFIR) push the market toward greater interoperability, which can make purely closed-loop models harder to sustain without platform changes. And “closed loop” doesn’t mean unregulated: in the EU, once transaction volumes exceed certain thresholds (e.g., €1m) or the programme starts to look more interoperable, regulators may challenge whether it still qualifies as a limited network, forcing a decision between tightening scope or moving toward a licensed model.

- Security and compliance limitations due to legacy technology. Many traditional closed-loop card programmes were built on older infrastructure, which can limit support for modern security standards (e.g., EMV chip, real-time fraud monitoring, PCI DSS alignment) compared to scheme-based open-loop systems.

- Lack of digital user experience (UX) and self-service features. This is partly because of legacy processing systems and because closed-loop programmes don’t benefit from scheme-standard features (e.g., no consistent support for Apple Pay or Google Pay).

- Harder and more expensive to expand acceptance. Adding new merchant partners, regions, or new use cases (e.g., EV charging, tolls, parking) often requires one-off integrations and commercial agreements. This makes expansion slower and more costly than in open-loop schemes.

Advantages and disadvantages of open-loop card payment systems

The advantages of open-loop systems that set them apart from closed loop include:

- Universal acceptance. One card covers multiple types of purchases, reducing admin work and increasing usage and transaction volumes.

- Easier to enable digital-first experiences. Open-loop cards follow scheme standards, making it easier to support digital wallets (e.g., Apple Pay, Google Pay), e-commerce, and card-not-present transactions consistently across markets.

- Regulatory compliance is already built into the card. Scheme-led systems are regulated, so they need to stay up to date on the latest requirements (e.g., AFIR), ensuring compliant, future-proof payments.

- Maintain controls even with broad acceptance. With a modern issuer/processor, you can enforce spend policies in real time using limits by category, location, and time, helping prevent off-policy purchases.

- A broader view of spend across merchants and regions. Open-loop acceptance gives you visibility into customer spend beyond a single private network. The depth and structure of reporting still depends on your issuer/processor and the data available from merchants. But with broader usage you can spot patterns like category-level spend, regional trends, and duplicate vendors more easily. Closed-loop can capture richer item-level data in supported environments, while open-loop typically improves breadth of coverage.

However, traditional open-loop systems also have their own challenges:

- Regulatory and scheme governance overhead. Moving into open loop often means taking on additional regulatory burden (or partnering with a licensed entity), alongside scheme rules and reporting requirements.

- Heavier onboarding and compliance checks. Open-loop programmes typically require stronger customer due diligence and ongoing AML/CTF controls, which can add friction to customer acquisition and increase operational workload.

- Potential licensing uplift for credit propositions. If your programme expands from payments into credit, some markets require additional authorisations (or a licensed partner), increasing governance and operational complexity.

- Higher fees. You’ll deal with transaction, interchange and processing fees through the card schemes, which can weigh heavily on low-margin companies like fleet operators that own their vehicles.

- Fraud and dispute operations at scale. Broad acceptance increases exposure to fraud and chargebacks (especially in e-commerce and card-not-present use cases), so open-loop programmes need stronger risk controls, monitoring, and operational capacity, which adds cost and complexity.

- Limited controls and data. You can’t set up restrictions as easily as closed-loop systems, and the data received may not be enough to sufficiently analyse end-customer behaviour and therefore block fraud.

6 top use cases for open-loop card payment systems (and when to use them)

Open-loop card systems vary in their use cases. We cover the top six below.

1. General-purpose payment cards where wide acceptance is key

For banks and neobanks, open-loop payment systems are the default way to deliver broad acceptance, but the real differentiator is how well that acceptance scales across markets, compliance regimes and customer segments.

An open-loop system for financial institutions increases card usage as well as issuer profitability by:

- Driving higher transaction volumes due to its wide acceptance with more interchange revenue

- Enabling more cross-border spend which means more FX revenue

- Supporting cash access, which means more ATM-related fees

- Improving customer retention and upsell opportunities (e.g., premium tiers).

Even institutions with established card programmes increasingly migrate to modern open-loop issuing and processing infrastructure to improve agility, data quality, and operational resilience as products and markets expand.

This helps legacy institutions remain competitive against challenger banks by speeding up time-to-market for modern features (like mobile wallets, contactless payments, real-time controls, and faster onboarding) while reducing technical and infrastructure complexity and supporting evolving compliance requirements.

2. Fintechs offering corporate expense management solutions with significant mobility spend

For most expense management providers, open-loop cards are already the default because employees need to pay anywhere business happens. The differentiator comes when mobility spend becomes a major category (fuel, charging, tolls, parking, car rental), where firms may need stronger controls, better data, and VAT-ready workflows than a general expense card typically supports.

This is why some providers add fleet-focused products (e.g., scheme fleet programmes) alongside their core expense card to better serve mobility-heavy customers.

With a single card, employees and contractors can make a wide range of work-related purchases. When mobility spend becomes a major category (fuel/charging, tolls, parking, car rental), it often increases transaction frequency, cross-border usage, and the need for tighter controls and richer data than traditional expense categories.

Open-loop cards appeal to high-spend companies wanting a unified payment card covering both mobility and other corporate expenses. By offering cards that are widely accepted globally, fintechs expand their value proposition and the volume of their customers’ transactions, while improving their customer relationships.

At scale, the challenge for expense platforms isn’t issuing cards, but maintaining control, compliance, and structured data as mobility spend increases.

3. Fleet/fuel/mobility programmes needing wider acceptance than any single network

For years, fuel retailers relied on closed-loop payment systems to restrict fuel and charge cards to specific networks, optimising pricing, loyalty, and control within a predictable environment. Now, as fleets become hybrid and regulations like AFIR mandate open-loop card acceptance at fast-charging stations, payment infrastructure must evolve beyond single-network models.

At the same time, schemes are starting to close the gap with fleet-focused products, but full capability still depends on merchant and acquirer adoption.

We can see this shift through the fact that the European fuel card market is projected to grow from $387.05bn in 2025 to $581.94bn in 2033, with open-loop cards expected to see a compound annual growth rate (CAGR) of 12.3% during the same forecast period.

An open-loop card allows cardholders to buy across multiple fuel stations, EV charging networks, and mobility services, enabling fleet and mobility firms greater operational efficiency and future scalability by expanding into new regions and adding new acceptance partners without launching separate card networks.

For example, consider a fuel card issuer running a closed-loop card that’s primarily accepted across its own branded sites. If it wants to expand acceptance beyond its retail network – adding independent stations, EV charging partners, tolls or parking – it often has to onboard partners one by one, negotiate commercial terms, and build/maintain separate integrations. That makes coverage expansion slower and more expensive than enabling scheme-based acceptance.

An open network provides them with a single payment system with a wide acceptance throughout Europe, allowing them to offer their services to these new regions more quickly and compliantly, without ending up with fragmented reporting, duplicated controls, and higher operational risk as new partners and regions are added.

4. EV charging and e-mobility where no single provider has enough network coverage

EV charging highlights the limits of closed ecosystems more quickly than fuel, as charging networks are fragmented, third-party owned, and increasingly regulated for open access.

But no single EV charging provider has enough charging locations across regions and key routes to serve all customer needs.

To serve diverse fleets, acceptance must be broader than a single provider’s network, without forcing fleets into multiple cards, apps, or fragmented reporting workflows. An open-loop card payment system can provide that flexibility.

Switching to an open-loop system makes sense when fleet and mobility programme providers:

- Have geographic expansion needs

- Begin diversifying with electric vehicles

- Change their commercial offerings, such as new partnerships

5. Hybrid programmes using closed loop for strict fleet controls and open loop for consumer/loyalty or broader spend

More fleet and mobility providers are using hybrid programmes. Here, “hybrid” means running both closed-loop and open-loop programme configurations on the same issuing and processing platform, depending on the customer segment or use case.

A hybrid approach built on a single issuing and processing foundation allows firms to:

- Maintain strict controls where they’re most critical (e.g., fleet operations requiring product-level restrictions like diesel-only purchases)

- Expand their value proposition to consumers with broader spending capabilities

- Serve different customer segments with different needs at the same time

For example, fleet-specific controls and routing can apply where required, while open-loop acceptance supports broader loyalty or consumer-style spending, all within the same programme infrastructure.

6. Fleet-grade open-loop card programmes

Fleet-grade open-loop card programmes combine open acceptance with fleet-specific controls that traditionally only closed-loop cards could support, such as

- Fuel-specific restrictions

- Full receipt and line-item data

- Support for VAT invoicing workflows (e.g., invoice-on-behalf, and settlement bypass)

- POS prompting (e.g. vehicle/driver ID, vehicle mileage)

The key capabilities are the ability to restrict purchases at a granular level (similar to closed-loop restrictions) and to receive richer transaction data (e.g., Level 2/Level 3 and line-item/receipt data), while allowing greater acceptance.

For example, Visa Fleet 2.0 is an enhanced Visa product that offers these capabilities, so issuers can place these restrictions and get visibility on exact products, quantities, and VAT rates.

However, for this type of programme to work, both merchants and acquirers need to support Visa Fleet 2.0, hence why it’s still not a widespread use case. And beyond the technical layer, some fleet use cases (like consolidated VAT invoicing) may still require bilateral agreements with fuel retailers or, alternatively, workflows such as receipt capture and expense management tools to support bookkeeping and VAT reclaim.

No matter the use case, your transition from closed to open-loop (or even taking a hybrid approach) is a gradual process. And it doesn’t mean abandoning closed loop. Enfuce helps financial institutions, fintechs, and fleet and mobility operators navigate this change with scalable solutions with compliance built in, whether you stay closed loop, go open loop, or run both.

Why partner with Enfuce to enable an open-loop card payment system

Enfuce is an all-in-one platform for next-generation card issuing and payment processing.

Founded in 2016, Enfuce is one of Europe’s top payment providers present in Europe and the UK, and with a footprint in South America. With our variety of payment methods that include debit, prepaid cards, and credit cards, traditional banks, neobanks, fintechs and fleet and mobility firms can create custom experiences for their end users now and scale them into the future.

Here is why leading organisations like Octopus Electroverse, OKQ8, and Fleet 220 use Enfuce’s open-loop card payment system to future proof their programmes:

1. Enable both open and closed-loop card payment systems through a single issuer

If you want to be able to offer different types of cards to different types of customers, usually it requires integrating several card providers to combine broad acceptance with industry-specific controls and invoicing. This is especially true in the fleet and mobility industries, where mixed fuel needs and interoperability requirements are growing.

But a multi-provider approach creates technical and operational complexity, with multiple contracts, integration maintenance, data gaps, and unclear ownership.

With Enfuce, you solve this by running open-loop and closed-loop programmes through a single issuer and platform. A single integration and set of controls enables you to launch new card products faster and manage:

- Cardholder onboarding and lifecycle

- Spend controls and limits

- Reporting and reconciliation

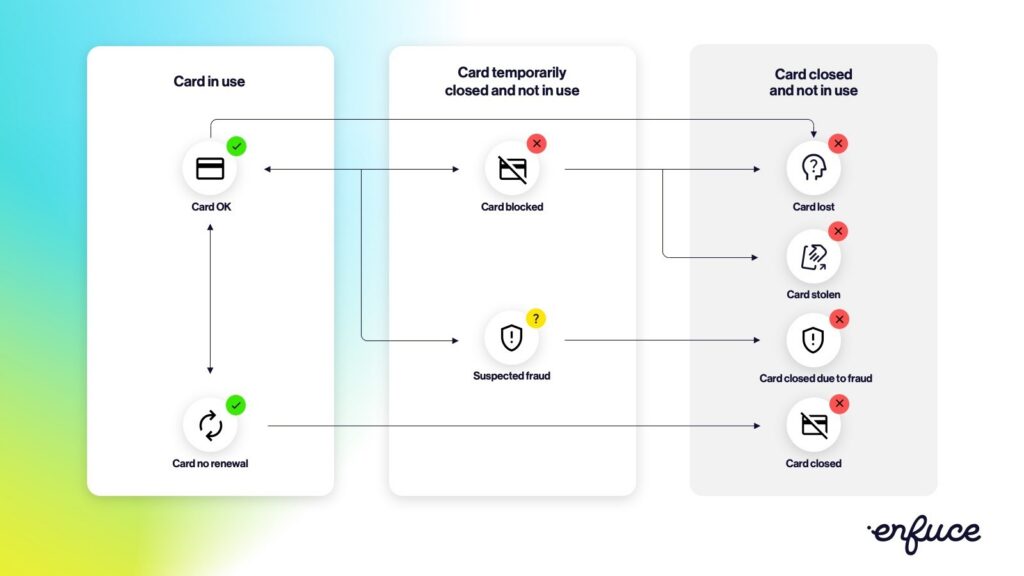

An example of your card lifecycle flow in Enfuce

Enfuce enables you to support different payment propositions for different user segments, without fragmenting your underlying card infrastructure, such as:

- Corporate fleets that need tight fuel controls and operation workflows

- Employees and travellers who need broad, open-loop acceptance for high-spend mobility expenses

- Loyalty and consumer programmes that benefit from scheme-level reach without custom integrations

Your end customers experience a single, consistent app or portal, even when open-loop and closed-loop logic coexist behind the scenes. And if you prefer different experiences for different segments (e.g., fleet operators vs. consumers), you can still build separate portals on the same Enfuce APIs.

Caption: Enfuce enables rich data insights on your card programme

Instead of reconciling multiple vendor files, Enfuce allows you to consolidate open- and closed-loop transactions into a single data model.

This unified view supports analytics, fraud and risk monitoring, finance operations and dispute handling, without duplicating processes across providers. You also simplify your relationship management by reducing contracts, support queues, dispute handling complexity, accountability gaps, including scheme-level responsibilities.

With Enfuce, you can even start with a closed-loop card programme (e.g., where fuel-specific controls are critical) then expand to open loop as customer needs broaden (e.g., EV charging, parking), without rebuilding integrations or operations from scratch.

Curious to know more about Enfuce’s open-loop card offering? Check out our API docs and reference guides.

2. Remain compliant without affecting the end-customer experience as you migrate from closed to open loop

You may see the value of moving to an open-loop model, but new scheme rules, regulatory requirements, and operational change can raise concerns about cost, delivery risk, and customer disruption.

For fleet and fuel operators in particular, moving to open-loop card issuing introduces obligations such as PCI DSS, PSD2 and Strong Customer Authentication (SCA) along with the learning curve that comes with operating in a scheme environment.

Addressing these requirements for the first time often slows programmes down, especially when compliance, operations, and product design are tackled in parallel.

Enfuce removes that burden by acting as an issuer-grade partner with an open-loop-ready platform. As an Electronic Money Institution (EMI) authorised in the UK and EEA, we also offer BIN sponsorship, allowing you to outsource core compliance requirements and launch with confidence.

For operators outgrowing limited-network models, partnering with a licensed issuer can reduce regulatory burden while preserving flexibility, whether you stay closed loop, go open loop, or run both.

Our cloud-based platform ensures a safe, smooth migration without disrupting your fleet operations or customer experience. Compliance is built into the programme design and day-to-day operations, so you don’t have to juggle a separate transformation project. This allows you to stay focused on your core business.

In practice, we turn your regulatory requirements into concrete programme rules, operating processes, and technical implementation. This means you meet scheme expectations from day one while not worrying about common compliance-driven pitfalls (e.g., designing controls, data flows, and operational processes) that cause delays.

With Enfuce, you also operate under a consistent compliance framework for closed loop, open loop, or both. This means you won’t need to reinvent policies and processes when you expand to new regions, merchant types, or product types, like EV networks.

For example, Europe’s largest EV network, Octopus Electroverse, turned to Enfuce when it needed greater flexibility in fleet electrification without compromising on compliance.

With Enfuce’s built-in spend controls, Octopus Electroverse offered restrictions based on location, merchant category, or time of day to prevent misuse and improve cost control. Enfuce also handled complex back-end requirements like BIN sponsorship and regulatory support, while Octopus Electroverse maintained ownership of the brand, customer experience, and customer relationships.

This allowed Octopus Electroverse to expand fleet electrification use cases without introducing compliance risk or operational fragmentation.

Discover more about Octopus Electroverse’s compliant open-loop solution

3. Receive support from experts who understand fleet/fuel/mobility use cases

Many open-loop card processors are optimised for retail banking and neobanks, rather than fleet, fuel, or mobility-specific use cases. So, when fleet/fuel/mobility operators ask for fuel-specific controls, VAT workflows, or mixed open and closed-loop programmes, they hit a knowledge gap with generic third-party card issuers and spend weeks translating fleet-specific requirements into generic payment terminology.

Enfuce is different. Not only will you have access to Visa 2.0 as one of our main partners, you’ll be paired with a fleet-focused platform and domain experts who understand your industry and guide you from discovery through launch. This avoids educating your processor partner from scratch and receiving solutions that don’t match your business needs.

Our teams are experienced in fleet-specific controls, acceptance realities, and invoicing requirements, meaning less time explaining edge cases, and more time building the right proposition.

You’ll have our expert support as you shift from closed-loop to open-loop programmes as we combine:

- Technical delivery on how to migrate, implement and operate your open-loop system

- A compliance/issuer perspective so you know how to migrate safely and correctly

- Business context to see how your solution maps to your customer segments and revenue model

Our domain experts also guide you in deciding:

- What should be open loop, closed loop or both

- Where restrictions are feasible

- What dependencies exist in the payment ecosystem (e.g., merchant/acquirer readiness for enhanced fleet features)

This reduces discovery risk and shortens the path from concept to compliant launch.

With Enfuce, you’ll create a card proposition that aligns with actual end-customer behaviour and operational workflows based on your use case, from trucking fleets to mixed fuel+EV charging.

If your fleet requirements conflict with generic open-loop limitations, our teams help you spot these early, instead of discovering them late during implementation.

How OKQ8 migrated from closed to open-loop payment system leading to increased transaction volume with Enfuce

OKQ8, one of Scandinavia’s largest fuel companies, partnered with Enfuce to modernise its card issuing and support its shift toward sustainable mobility.

Enfuce provided a unified, cloud-native issuing and processing platform to consolidate OKQ8’s open-loop scheme cards and closed-loop private/fleet card programmes under a single back end. To start, OKQ8 successfully launched a new Visa-branded credit card programme (starting with Visa Credit) with no go-live issues. Our API-focused architecture enabled rapid scaling while simplifying future product expansion.

The second phase was the broader modernisation project. Enfuce supported the migration of OKQ8’s existing closed-loop fleet cards to open-loop Visa-branded credit and debit cards. By expanding where cards could be used, OKQ8 increased their transaction volumes and supported customer needs beyond their own brand to include EV charging, Green Fleet, and clean energy services across Sweden and Denmark.

The transition was phased and coexistence-friendly, allowing legacy and evolved card logic to operate in parallel during the migration.

The evolution also strengthened OKQ8’s compliance. Enfuce’s platform is designed to meet strict regulatory and industry standards, including PSD2 alignment, FIN-FSA approval, and PCI DSS Level One compliance, providing a scalable issuing solution out of the box.

Enfuce’s hands-on partnership, including technical expertise and best-practice guidance throughout the transition, helped OKQ8 innovate its payments capabilities as it digitalises and pivots from fossil fuels toward sustainable mobility.

Learn more about the Enfuce-OKQ8 partnership: OKQ8 partners with Enfuce around card issuing modernisation, in their transformation towards sustainable mobility

Upgrade your card payments to open-loop with Enfuce

While closed-loop systems still play an important role, open-loop and hybrid card programmes are increasingly necessary to meet regulatory, geographic, and customer expectations. It helps consolidate multiple offerings into one card programme if you’re a fintech, expand into different regions and diversify purchases if you’re a fuel card provider, and expand to new charging stations if you’re an EV charging or mobility operator.

At Enfuce, we provide a flexible, scalable approach, helping financial institutions, fintechs and fleet and mobility operators gradually transition from closed-loop to open-loop while maintaining security, compliance, and cost control.

Want to take the next step? Learn how Enfuce’s open-loop and hybrid payment solutions can simplify your payments, enhance security, and future-proof your business. Get in touch today!

FAQs on open-loop card payment systems

1. What’s the difference between closed vs. open-loop card payment systems?

The difference is in their restriction and acceptance levels. Closed-loop card payment systems are issuer-led and restricted to specific payment networks and merchants. Open-loop systems are scheme-led and more flexible, allowing cardholders to make purchases with merchants that accept the scheme anywhere in the world.

2. When does it make sense to use an open-loop payment system?

Open-loop payment systems make sense when you need to expand to new regions or merchants, enhance the customer experience with wider acceptance, set up new partnerships that boost your value proposition, future proof your payment systems, or need to keep up with the competition.

3. What are some examples of open-loop card systems?

Open-loop card system examples include corporate mobility cards, digital wallets, expense cards, gift cards, employee benefit cards and even fleet-specific cards like Visa Fleet 2.0.

4. As a fleet operator, can I get open-loop acceptance without losing closed-loop-like controls?

Yes. With fleet-focused card issuers like Enfuce, fleet operators can adopt a hybrid approach that allows them greater acceptance flexibility while still maintaining closed-loop like controls. For example, Enfuce’s partnership with Visa 2.0 enables fleet operators to place fuel-specific restrictions and wider merchant acceptance, while having item-level visibility on transactions.

5. What do I need to launch an open-loop card programme?

You need compliance with regulatory (PCI DSS, PSD2/SCA, GDPR) and scheme (Visa/Mastercard) requirements to launch an open-loop programme. This includes scheme access and BINs, an issuing and processing platform with APIs, fraud and dispute operations, card production and personalisation, plus testing, pilot and go-live support with clear roles and governance in place. Outsourcing your compliance requirements to a licensed card issuer processor like Enfuce that also offers BIN sponsorship can help you launch your card programme fast and safely.