Issuer processor APIs: How they work, key use cases and what to look for.

As card programmes scale, issuer processor APIs are often explored to address familiar friction points like:

- Manual processes that slow down operations and create unnecessary overhead

- Limited automation across issuing and processing workflows

- Difficulties scaling programmes across multiple markets

- Growing complexity in staying compliant with evolving regulations

In most cases, these issues can be traced back to legacy infrastructure that struggles to keep pace with volume growth and adapt to market changes. These systems make automation difficult, limit real-time control, and slow down innovation.

That’s where issuer processor APIs come in. They offer a practical way to upgrade your issuing and processing stack without rebuilding your entire infrastructure. Rather than requiring a full rebuild, they allow you to upgrade how your cards are issued and managed, automate transaction processing, and operate within a compliant, scheme-aligned infrastructure.

As an issuer processor with over a decade of experience, we at Enfuce have seen firsthand how APIs can improve the way card programmes are built and managed. To help you evaluate your options and choose the right APIs for your business, we’re breaking down the key capabilities, use cases, and what to look for in an issuer processor API provider.

Read on to find out:

- How issuer processor APIs work

- Issuer processor APIs by use case: Who benefits and what to look for

- Why companies choose Enfuce’s issuer processor APIs

- How Enfuce’s issuer processor APIs enabled Swile to scale 4+ million employee benefit cards across Europe and South America

- FAQs

Looking to upgrade your card programme? Get in touch with our team.

How issuer processor APIs work

Issuer processor APIs connect directly to your product, giving you access to the tools and systems required to issue cards, manage card programmes, and process card transactions. This includes the ability to:

- Create and manage customers, accounts, and cards

- Define and enforce authorisation rules

- Process card transactions

- Enable digital wallets

- Configure spend controls

- Receive real-time transaction and authorisation notifications and real-time data

Issuer processor API example

Here’s a quick example of how issuer processor APIs by a platform like Enfuce handle the full card issuing and transaction processing cycle:

- Card issuance: You create customers and accounts in Enfuce’s system via our API, then trigger card issuance via an API request, which defines the key card attributes. Enfuce creates the card, applies programme rules, and makes it immediately usable.

- Transaction initiation: The cardholder uses the card, triggering the processing flow.

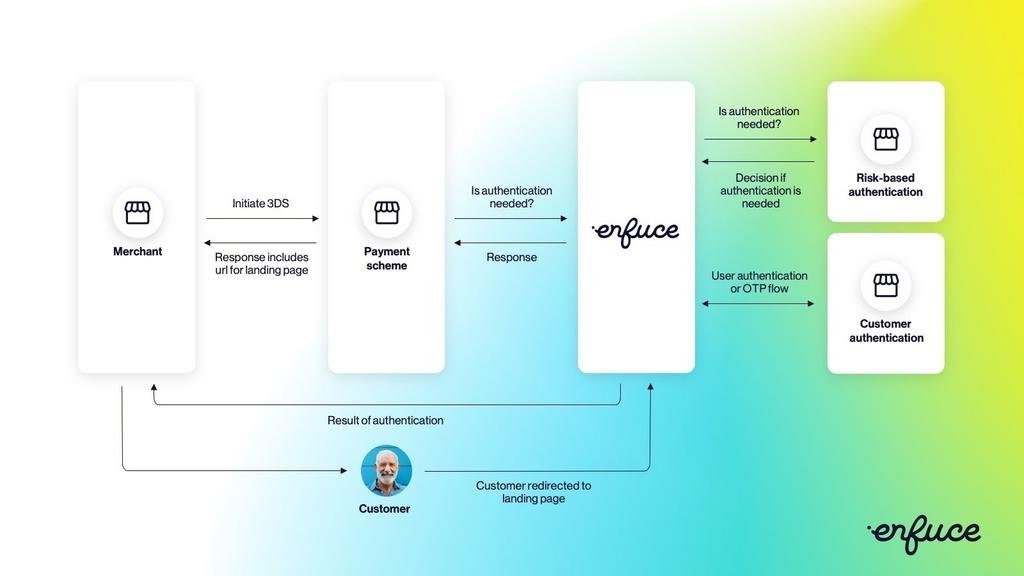

- Authorisation: The merchant sends an authorisation request via the card network, which Enfuce evaluates across three layers. Enfuce may handle all or some of these steps:

- Technical validation: Security elements in the authorisation message are checked against data and keys. If technical validation fails, the authorisation is declined.

- Business validation: Transactions are verified against rules you or your customer set, such as spend controls. If business validation fails, the authorisation is declined.

- Fraud validation: The transaction is then screened for fraud, either by Enfuce’s fraud monitoring system or an external provider. Enfuce also confirms whether customer authentication has been performed.

- Customer authentication (when required): For certain transactions, authentication is required under PSD2 or card scheme rules. Online cards are enrolled in 3DS for risk-based authentication; in-store, the merchant decides whether authentication applies.

- Authorisation response: Enfuce returns an approval or decline in real time, signalling to the merchant to either complete or stop the transaction.

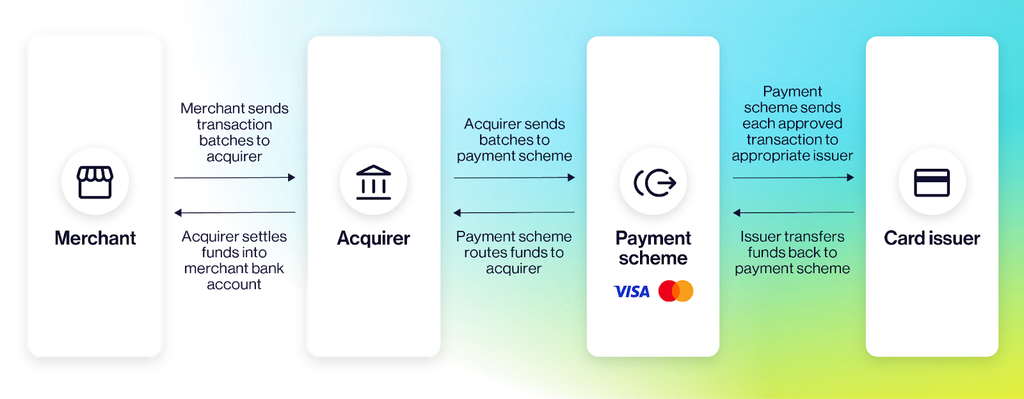

- Clearing and settlement: Approved transactions are sent by schemes (Visa, Mastercard) up to six times a day. Enfuce automatically processes each batch, posting transactions to cardholder accounts, applying fees, updating account balances, and routing funds through the schemes to the merchant.

As you can see, issuer processor APIs go beyond a basic card-issuing API by supporting the entire card lifecycle, not just the initial issuance step. Want to dive deeper into how a card issuing API works? Check out our article, Card Issuing API: How to scale your programmes compliantly.

Issuer processor APIs by use case: Who benefits and what to look for

Card issuer processor APIs can be used across a wide range of industries. Below are a few common use cases, along with the key capabilities to look for in an API for each.

1. Banks, fintechs, and digital-first lenders

Banks, fintechs, digital-first lenders, and financial institutions can use issuer processor APIs to issue prepaid cards, debit cards, and credit cards to their customers while supporting real-time spend controls and end-to-end transaction processing, and handling complex credit logic and regulatory requirements as you scale. These APIs make it easy to connect to your core banking and quickly launch and iterate your card products, reducing time to market. They also keep risk controls, reporting, and compliance consistent as you scale.

Key API capabilities to look for:

- Configurable billing cycles, interest calculation logic, grace periods, minimum-to-pay (MTP) rules, and payment allocation priorities per product or segment

- Flexible credit models supporting revolving credit, charge cards, and post-purchase instalments plans

- Automated, compliant invoicing to stay audit-ready across jurisdictions

- Real-time visibility into balances, delinquency status, and account-level write-offs

- Structured General Ledger and Data Warehouse exports for accounting and reconciliation

- API-driven configuration to adjust credit limits, MTP percentages, billing settings, reminder flows, and repayment parameters programmatically

2. Fleet and mobility providers

Fleet and mobility providers increasingly need to build card programmes that support diverse payment scenarios, such as fuel, EV charging, tolls, and other vehicle-related services, often across borders. With APIs, you can enforce fuelling and charging spend controls in real time across merchants and countries, reducing leakage and fraud without slowing drivers down.

Key API capabilities to look for:

- Hybrid fleet cards that work across fuel, EV charging, and multimodal mobility

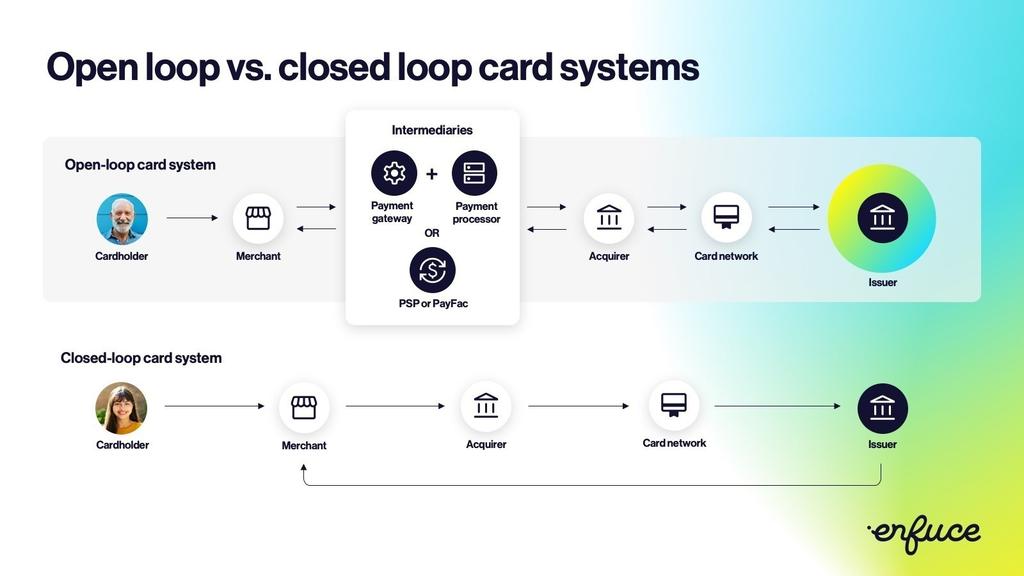

- Granular spend controls by merchant, category, location, or even specific product

- Support for open-loop, closed-loop, and hybrid acceptance models

- Real-time spend visibility to spot unauthorised or out-of-policy usage

- Fraud protection against fuel fraud, skimming, and unauthorised spending

- Multi-country and multi-currency capabilities for cross-border travel

3. Employee benefit companies

Employee benefit providers and programme managers use issuer processor APIs to build flexible, multi-category benefits programmes, delivered through physical and virtual payment cards.

Instead of relying on fragmented vouchers or closed-loop systems, providers can consolidate meal, mobility, wellness, and other benefits onto one scalable card infrastructure, ensuring real-time controls, tax-compliant spend rules, and seamless user experiences for both employers and employees.

Key API capabilities to look for:

- Multi-PAN functionality to support multiple benefit categories (e.g., meals, mobility, wellness) on a single card while keeping balances and compliance rules separated

- Real-time spend controls to enforce tax and regulatory rules by merchant category, location, time, or budget

- Open-loop card acceptance for broad usability across Visa and Mastercard networks and easier operations

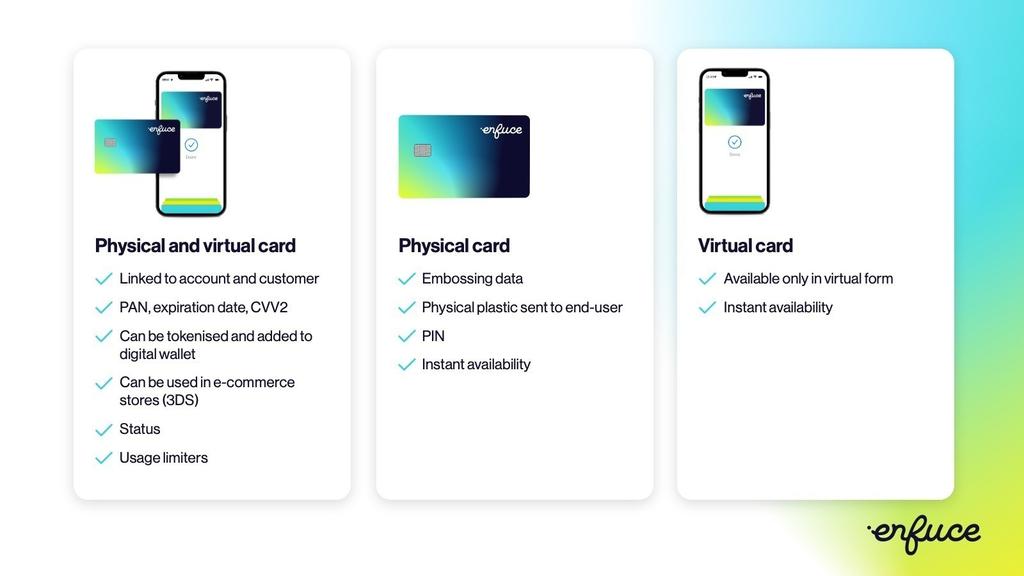

- Instant issuing of physical and virtual cards with digital wallet tokenisation

- Real-time reporting and unified ledger visibility for employers and finance teams

- Custom branding options for card design and programme identity

- Multi-country and multi-currency capabilities to support cross-border benefit programmes

4. Expense management platforms

Expense management solutions could use issuer processor APIs to issue and manage corporate cards for their customers, enabling real-time spend visibility and automated reconciliation across teams and markets.

By embedding card issuance and transaction processing directly into their platform, they can streamline expense workflows, reduce manual handling, and give finance teams accurate, up-to-date oversight of company spend.

Key API capabilities look for:

- Instant issuing of physical and virtual corporate cards, with digital wallet support

- Real-time transaction data and authorisation controls to manage spend by merchant category, geography, or limit thresholds

- Configurable spend limits and usage rules aligned with company spending frameworks

- Live transaction data for up-to-date expense visibility

- Account hierarchies to manage teams, budgets, and cardholder permissions

- Multi-country and multi-currency support to support international expansion

- Automated settlement and reconciliation support via structured data exports

5. Non-profits and governments

Programmes distributing aid or benefits often need to move funds quickly while maintaining strong oversight and fraud prevention. Issuer processor APIs make it easier for non-profits and governments to issue cards, oversee how aid funds are used, and catch misuse early.

Key API capabilities look for:

- Configurable spend rules to restrict usage by category or merchant

- Real-time card issuance (physical and virtual), including digital wallet tokenisation

- Real-time access to customer and card data for operational teams

- Built-in fraud monitoring and case management to minimise misuse

Why companies choose Enfuce’s issuer processor APIs

Across industries, these use cases share a need for fast, flexible, and compliant card issuance, real-time controls, and actionable insights – capabilities that issuer processor APIs make possible.

Enfuce combines regulated card issuing, BIN sponsorship, and issuer processing in one secure and scalable API-first platform. Our modular API-based platform enables you to issue and manage physical and virtual cards across credit, debit, prepaid, and specialised programmes (such as banking, fleet or employee benefits), while handling authorisation, clearing, settlement, and lifecycle management end-to-end.

Here’s what you can do with Enfuce:

Future-proof issuing and processing with an API-first platform

Legacy platforms often require frequent updates as card schemes evolve, new features and functionalities emerge, and regulatory requirements change. Those updates come with downtime and manual workarounds, which can frustrate users and make reliability harder to guarantee at scale.

Enfuce’s API-first, cloud-native platform is designed to handle the full lifecycle of card issuing and payment processing without these limitations. Our modular architecture allows services to evolve independently, helping you introduce new features and regulatory updates without major system overhauls.

Caption: Handle the full lifecycle of card issuing and processing with Enfuce

Our APIs are well-documented, use-case driven, and designed as the primary interface for your operations. Your developers can explore our APIs in a dedicated sandbox environment, including endpoints such as Card details and Transaction Details, before moving to production.

From a performance standpoint, Enfuce delivers 99.999% uptime. We use Stand-In Processing (STIP) to ensure transactions can still be authorised during downtime, helping card programmes keep running even when systems are temporarily unavailable.

Tenant isolation adds another layer of resilience by physically separating customer environments, meaning heavy traffic or issues affecting one tenant are unlikely to impact you. This approach also reduces the risk of misconfiguration and unintended data exposure.

Scale across markets and volumes with a single partner

Expanding into new countries means dealing with local BINs, schemes, KYC requirements, currencies, and invoice formats. Without the right infrastructure, this can lead to fragmented setups and inconsistent processes.

Enfuce’s cloud-native, API-first platform comes with pre-built multi-country and multi-currency capabilities, so you can expand without rebuilding infrastructure or vendor stacks. You’ll also have support for local BINs and scheme requirements, with KYC/KYB and customer activation aligned to local regulatory needs.

As your programme grows, Enfuce scales with it. Our platform supports you no matter your growth stage – from early-stage programmes to millions of cards – handling thousands of transactions per second without compromising performance. By working with a single issuer processor, you can manage increasing volumes through one unified system, rather than juggling multiple providers as demand ramps up.

Scaling successfully also requires local expertise. With over a decade of experience, 150+ experts, and operations across Europe, the UK, and South America, Enfuce combines technical scalability with deep knowledge of different market requirements and regulations, helping you launch, expand, and operate confidently across borders.

Get built-in compliance and fraud prevention with a regulated provider

Compliance and fraud prevention are non-negotiable in card issuing, but managing them in-house is costly and complex. Requirements evolve constantly and vary by market, making it difficult to stay compliant while continuing to build and scale your product.

Enfuce is backed by the licenses, certifications, and operational capabilities required to issue and process cards at scale. With our BIN sponsorship, you don’t need to obtain or maintain your own Electronic Money Institution licence or card scheme membership.

We’re compliant with PSD2, GDPR, and CBPR, and are assessed annually for PCI DSS Level 1 and PCI 3DS certification. Enfuce also operates as your processor and facilitator in the 3DS flow, enrolling cards automatically during creation and handling authentication requests directly with the schemes.

You can also choose our dispute management and a fully managed, 24/7 fraud prevention service as part of our modular platform. This helps reduce fraud rates, supports your customer service team, and ensures disputes are handled in line with scheme rules and regulatory requirements.

Grow with hands-on support and flexible infrastructure

Choosing an issuer processor is about finding a partner that can support you into the future. Robust APIs are essential, but expanding a card programme also requires structured onboarding, migration support, and ongoing optimisation, improving the customer experience.

Enfuce combines API-first infrastructure with end-to-end customer support. During onboarding, our dedicated team helps configure your service and guides you through launching your card product. Once live, a customer success team and your dedicated customer success manager stay involved to ensure you’re getting the most out of our APIs as your needs change.

Our modular nature means you can start with what you need today and expand over time. You only pay for the services you use. That means you can avoid large upfront investments while still having the flexibility to add features, markets, or complexity later.

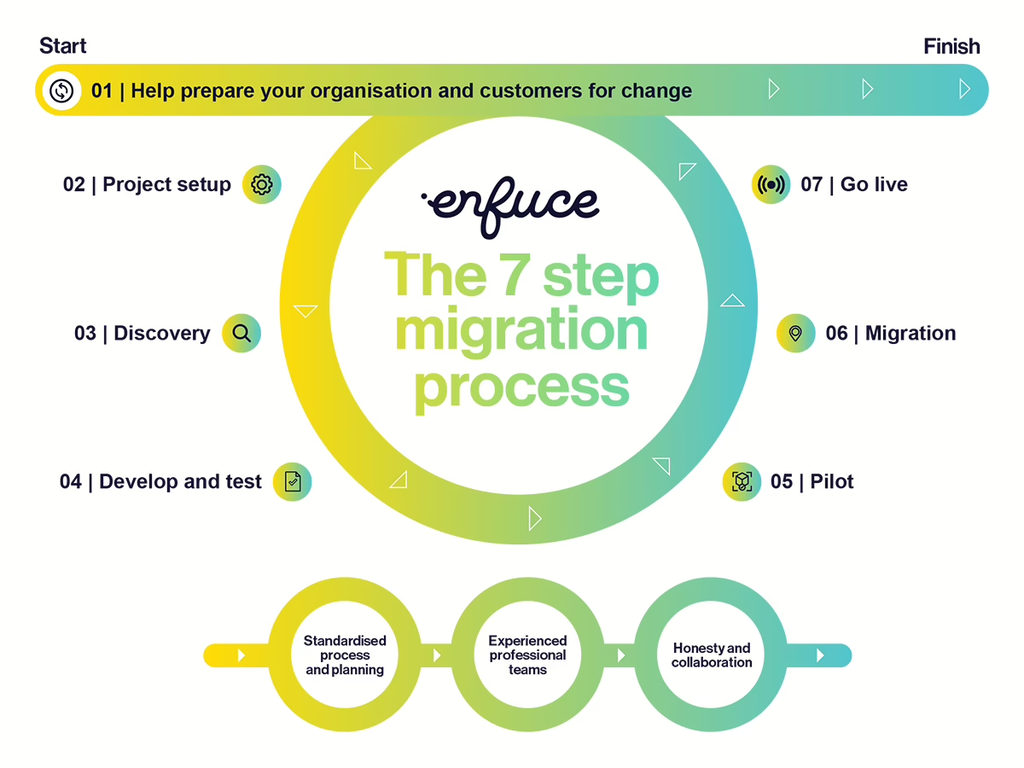

For those migrating from a legacy provider, Enfuce offers a structured seven-step migration framework. We work closely with you to migrate existing logic, value-added features, and operational workflows, all while identifying opportunities to improve performance and reduce internal operational load.

How Enfuce’s issuer processor APIs enabled Swile to scale 4+ million employee benefit cards across Europe and South America

Swile is a leading player in France’s employee benefit market, processing over €3 billion in transaction volume per year. After digitalising lunch vouchers, Swile set out to unify meal, mobility and culture benefits into a single, scalable card programme.

To do this at scale, Swile partnered with Enfuce to consolidate multiple benefits onto one physical card using a unique multi-PAN architecture. Each benefit is linked to its own balance and routing logic, enabling compliant handling of VAT rules, scheme requirements, and spend restrictions within one unified user experience.

Through Enfuce’s issuer processor APIs, Swile was able to issue physical and virtual cards, enable digital wallet tokenisation, manage authorisation and settlement flows, and support complex benefit-level spend controls, all within one scalable infrastructure.

The programme was designed to onboard over three million users in France, transforming how employee benefits are issued and managed across the country. Bilal Aslam, Global Head of Card Issuing at Swile, described the collaboration:

“This partnership with Enfuce marks the next chapter in our shared vision to fast-track the digital transformation of employee benefits. By combining Swile’s human-centric innovation with Enfuce’s world-class payment infrastructure, we’re setting a new global standard for how benefits are delivered and experienced.”

Building on the success in Western Europe, Enfuce’s infrastructure soon laid the foundation for Swile’s expansion into Brazil. All new Swile Brazil customers now get a combined benefit card, with over one million existing users expected to migrate to the upgraded card experience by mid-2026.

Learn more about how Enfuce’s issuer processor APIs helped Swile revolutionise employee experience management.

Simplify, secure, and scale your card programme with Enfuce’s issuer processor APIs

Running a card programme on legacy systems often means slow updates, manual processes, and operational limits when scaling across markets or expanding products.

Enfuce’s issuer processor APIs tackle these challenges head-on. They automate the full card lifecycle, provide reliable, cloud-native infrastructure, and include built-in compliance across jurisdictions. Scalability is built in, so you can expand across regions, currencies, and card types without rebuilding your systems or onboarding multiple vendors.

Beyond giving you access to our APIs, Enfuce works as a dedicated partner that guides you through migration, product launches, and ongoing optimisation, helping you get the most value from our platform. Whether you’re launching a credit card product, fleet programme, or employee benefit solution, we’re here to provide the tools and support you need to scale and future-proof your card programme.

Ready to see what Enfuce’s issuer processor APIs can do for you? Contact us today.

FAQs on issuer processor APIs

What is an issuer processor API?

An issuer processor API is a programmatic interface that enables businesses to integrate card issuing and payment processing directly into their systems. These APIs connect to core issuing and processing infrastructure, enabling automatic tasks such as card issuance, transaction authorisation, and clearing and settlement. Issuer processor APIs help reduce reliance on manual processes or legacy systems, which is why they’re used by banks, fleet and mobility companies, and other organisations to streamline card operations.

How does an issuer processor API work?

An issuer processor API connects your product to the systems that issue and process cards. Through API requests, you can create accounts, issue cards, define authorisation rules, and process transactions. Approved transactions are automatically cleared, settled, and routed to the relevant parties. Depending on the provider, issuer processor APIs may also support digital wallets, advanced spend controls, real-time notifications, and other capabilities.

What are the benefits of issuer processor APIs?

Issuer processor APIs simplify access to the infrastructure and certifications required for card issuing and processing. By automating workflows, they reduce operational complexity and enable faster programme launches. They also make it easier to scale across products, regions, and volumes, helping teams build and grow card programmes more efficiently.