Account

Account

The account entity’s main functionality is to hold the balance. It also functions as the link in case several cards share the same balance. For credit products, the account also represents the invoice level from which invoices are generated.

Parts of the account-level data are generic and collected for all product types. Some data fields are only relevant for specific products. Regardless of product, an account holds an account status, account properties, balance and available balance. For credit products, the account additionally holds a credit limit, technical balances (divided into different types of balances) and invoice generation data (minimum payment, interest, invoice delivery etc.), for instance. For debit products, an account holds the link to the bank account.

Below we list the fields of account-level data:

- Link to the customer that owns the account (customerId)

- It is required to link a customer to each account during account creation.

- Account balance (available, balance)

- See description below

- Address (address)

- An optional address can be set on the account level if needed e.g. for invoicing. The primary address resides on the customer entity.

- Account name (name)

- An optional name can be given to the account e.g. if it is a corporate account, the name of the company or department.

- Account number (number)

- An optional account number can be set when creating the account. This can be used e.g. if the issuer wants to generate a separate account number that can be linked to an internal system.

- Segment (segment) (optional service)

- As an optional service, the issuer can determine segments that can be used e.g. when determining fee levels.

- Payment reference (paymentReference)

- A number that can be used to process incoming payments for invoices.

- Number that links to an external account number e.g. in a core banking system.

- Credit limit (creditLimit)

- Determines the optional credit line that the customer has.

- Status (status)

- See the description below.

- Usage limiters (usageLimits)

- See the description here.

Account product types

See the documentation regarding account product types here.

Account balance and available amount

For products where the balance resides at Enfuce, Enfuce will keep track of the current balance and the available amount. The balance refers to the actual financial balance whereas available also considers possible pending authorisations. When determining the available amount during authorisation processing, usage limiters are also considered.

Example:

The account available amount is 100€ and the customer has a 50€ ATM per 24-hour limit.

The customer tries to withdraw 80€.

The authorisation is declined even though the available amount on the account is 100€ as the usage limiter limits the available amount for ATM withdrawals to 50€.

It should be noted that usage limiters are not accounted for in the available in the Account API (as the usage limiters are dependent on transaction type and conditions). See the below examples for further elaboration:

| Use case | Balance | Available |

|---|---|---|

| Customer tops-up with 100€ | 100€ | 100€ |

| 10€ authorisation posted | 100€ | 90€ |

| 10€ financial transaction posted (same transaction that has been authorised) | 90€ | 90€ |

| Customer withdraws 20€ from prepaid account | 70€ | 70€ |

See the transaction section for more information on how authorisations and financial transactions work.

The balance resides on the account level. If there are multiple cards linked to the same account, the balance is impacted by every card’s transactions. The available is likewise impacted by the account’s available balance, but when determining availability during authorisation processing, card-specific usage limiters are also considered and lead to differing amounts that can be purchased even when cards are linked to the same account.

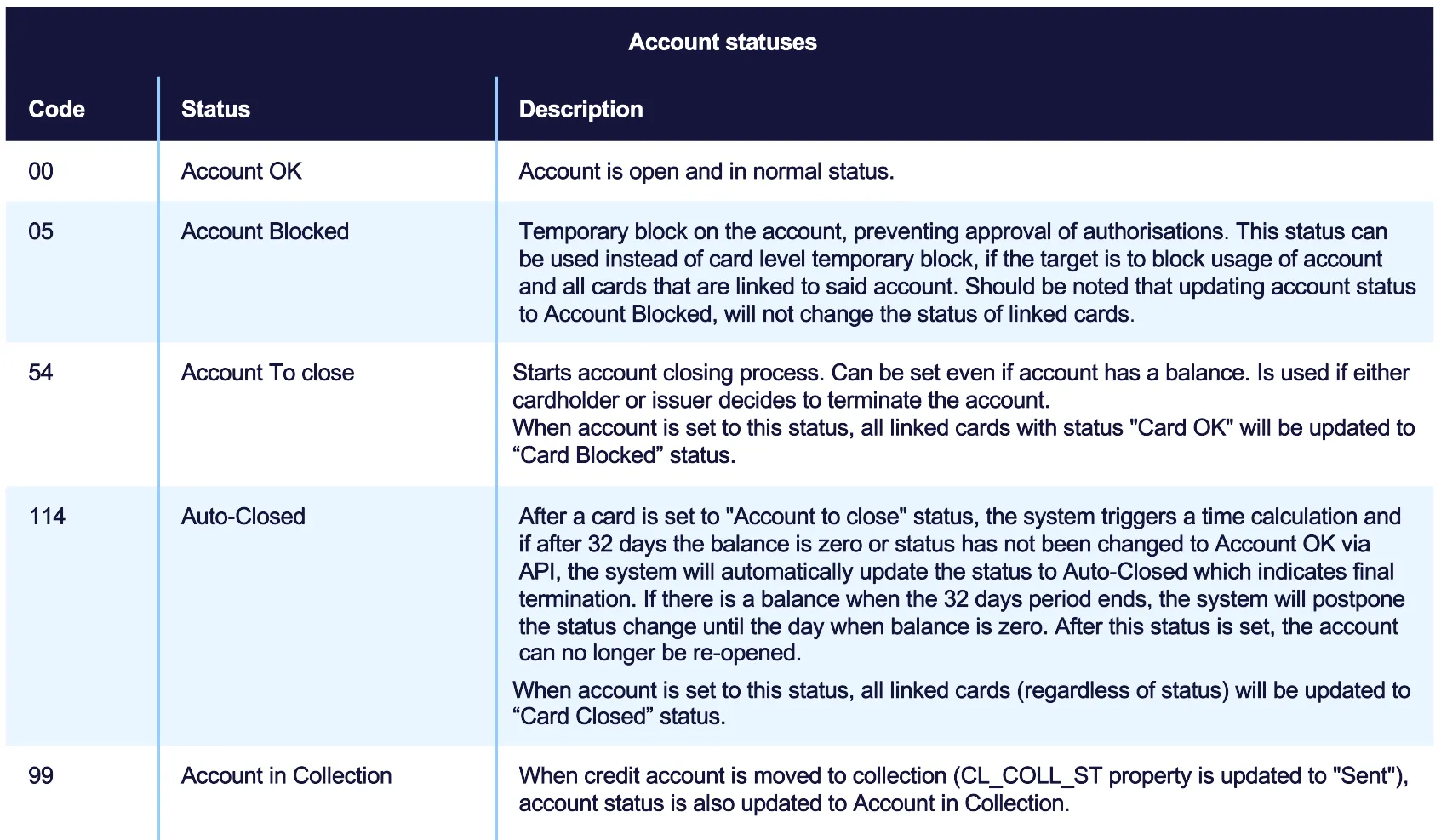

Account statuses

Account statuses present the status of an account at a certain point in time. The account has a higher priority than the card status which means that if an account is closed, it will impact all cards linked to the account. However, if a card is closed, it doesn’t automatically impact the account. Below is a list of account statuses:

Via the Enfuce Account API, the issuer can define a reason for the status change. The reason can be used e.g. to differentiate between changes that are initiated by the issuer and the ones initiated by the customer. The set reason is available in both view APIs as well as the Data export Account Properties file.

Account closing process

If the issuer or customer wishes to terminate the contract and close the account and linked cards, the account status should be updated via API to “Account to close”. Updating the account to this status will automatically update any cards linked to the account to “Card blocked” status. While these statuses prevent any further use, they still allow not yet posted financial transactions to be posted. This means that the termination can safely be done regardless of when the last purchase has been done with the card. Simultaneously, by having a period after termination to ensure that all transactions have been posted, prevents issues of failed transaction posting. There is a 32-day period which is considered a sufficient waiting time to consider any late transactions from merchants. “Account to close” / “Card blocked” statuses also allow to be reversed, i.e. if closing was done by mistake or the customer wishes to change their mind, it is still possible to do so within the 32-day period.

Assuming that the account balance is zero after the 32-day period, Enfuce will automatically update the account status to “Auto-Closed”. Updating the account to this status will automatically update any cards linked to the account to “Card closed” status.

Updating the account to Auto-Closed and cards to “Card closed” will mean the end of the accounts/cards being considered in the Enfuce monthly service billing. It should however be noted that service billing of account/cards will continue including the month when the account status is changed to Auto-Closed and card status is changed to Card closed. Example:

- The customer wishes to terminate the contract 10th of January → The account is set to “Account to close” and the card to “Card blocked”

- 11th of February the account balance is zero and the 32-day period has passed → The account is set to “Auto-Closed” and the card to “Card closed”

- As the account and card have been available to receive transactions in both January and February the issuer will pay for the service until February. Account and card will not be included in service invoicing in March.